US dollar-denominated sovereign bonds from the emerging world offer hefty returns and excellent diversification. (UBS)

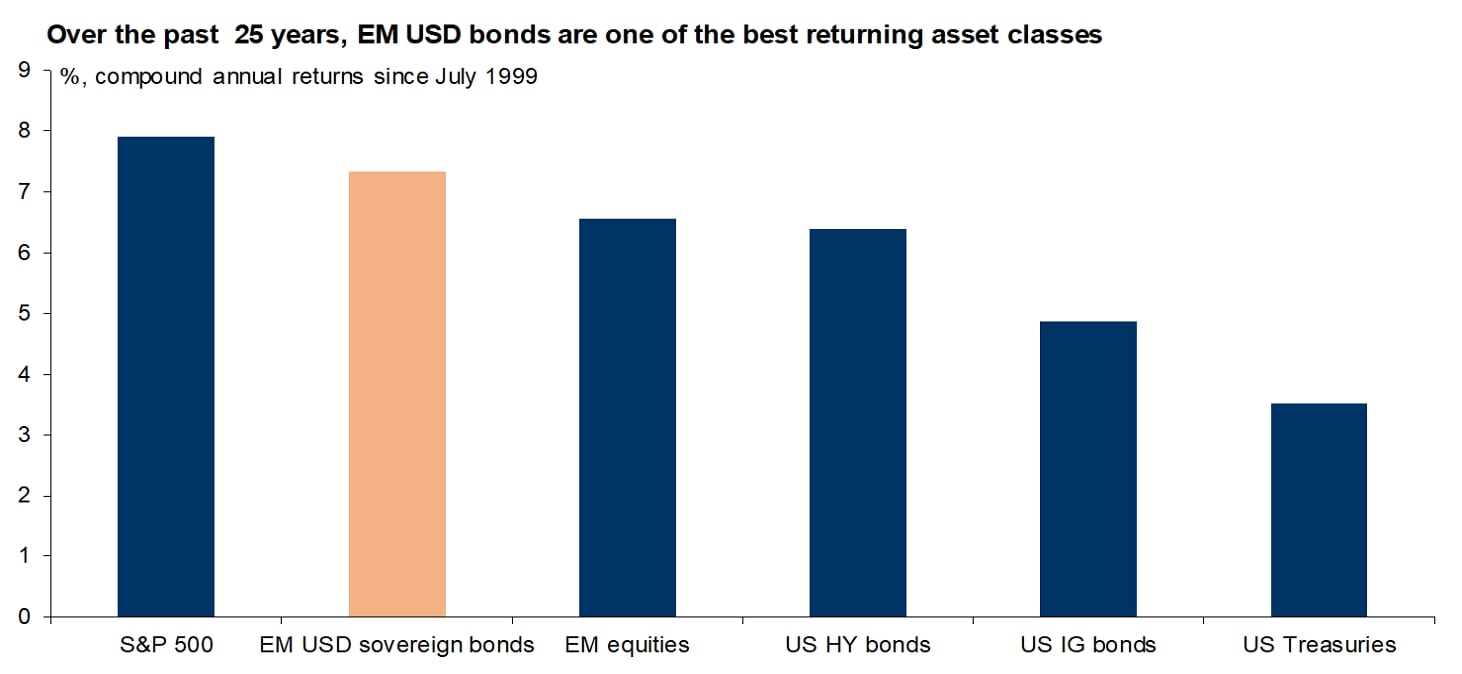

US dollar-denominated sovereign bonds from the emerging world—as measured by JP Morgan’s EMBI global index—have been one of the best-performing asset classes over the past 25 years. The asset class has provided compound annual returns of 7.3% since July 1999, barely below the 7.9% provided by the S&P 500, and well above the roughly 3.5% of US Treasuries.

What could be the reason?

The disconnect between performance and investor perception could be due to the relatively young nature of the asset class. Note that in the late 1980s and early 1990s, a large bulk of the emerging market countries—including large nations such as Mexico and Brazil—were part of debt restructurings under the Brady plan. It wasn't until the 2000s, with the implementation of inflation targeting and fiscal rules in several countries, that the emerging market bond asset class began to mature.

The emerging market investment universe has expanded dramatically in recent years, offering greater depth of choice to investors along with diversification benefits. Just two decades ago, a total of 30 emerging market countries had bonds outstanding in global markets of sufficient size and liquidity, but now there are more than 70. Moreover, the domain of emerging market bonds is also distributed much better geographically nowadays. While 20 years ago most issuers came from Latin America and Asia, the representation of countries and companies from Europe, the Middle East, and Africa has grown substantially, allowing investors to allocate capital across regions with ease.

Bottom line

As the world changes, investors should be vigilant and seize on opportunities others might miss. We think emerging market US dollar-denominated bonds are an overlooked outperformer, offering not only hefty returns but also excellent diversification. As of now, we expect emerging market US-dollar bond spreads to trend sideways over the next six to 12 months, allowing investors an opportunity to collect an appealing 7-8% carry (equity-like returns) and potentially benefit from capital appreciation as we enter a somewhat lower interest rate environment.

Please see our notes:

Investing in emerging markets: Political twists and turns, 24 July 2024

Demystifying emerging market bonds, 1 July 2024

Main contributor: Alberto Rojas, Investment Communications Writer — CIO Americas