Introduction

Sustainability is a multi-faceted topic, and climate and nature are two critical elements which are deeply intertwined and must be addressed together in the transition to a low carbon economy. As outlined in the Intergovernmental Panel on Climate Change (IPCC) Sixth Assessment Reports released in 2021 and 2022, achieving the Paris Agreement objectives requires a rapid transformation across the economy given that aggregate temperatures have already increased more than 1°C. The impacts of climate change are being felt already, as highlighted in studies such as the UK Government-sponsored The Economics of Biodiversity: The Dasgupta Review. It notes that the stock of natural capital per person has declined by 40% over the last thirty years. Land use change is one of the largest drivers of biodiversity loss and key ecosystems play a critical role in providing carbon sinks to help mitigate climate change as noted in the UN Environmental Program Emissions Gaps Report 2022 released at the 27th Conference of the Parties to the United Nations Framework Convention on Climate Change (COP27) in November 2022. Thus, increasingly climate and nature must be jointly addressed in order to meet the goals established by both the Paris Agreement and the Kunming-Montreal Global Biodiversity Framework agreed at the 15th meeting of the Conference of the Parties to the Convention on Biological Diversity (COP 15) in December 2022.

Similar to the financial world, where assets give rise to flows of revenue, the natural environment consists of stocks of assets (i.e., natural capital) that provide benefits to people and the economy (i.e., ecosystem services). As the transition to a low-carbon economy continues and reporting around climate continues to mature, it is important to remember that biodiversity is an essential characteristic of nature, critical for maintaining the quality, resilience and quantity of ecosystem assets and the provision of ecosystem services that businesses and society rely upon. These dependencies and impacts have been documented through a range of research initiatives including the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES)’Global Assessment Report on Biodiversity and Ecosystem Services, the IPCC’s Sixth Assessment Report 2021’s Fact sheet on Biodiversity, in addition to a variety of industry-led efforts. Hence, we recognize the importance of understanding human dependencies and impacts on nature, to better understand the transmission channels through which our clients and our firm may face risks and opportunities resulting from the dependencies and impacts of society’s activities on nature.

In 2022, we continued to progress on this journey toward a low-carbon economy, including through our continued implementation of the recommendations laid out by the Task Force on Climate-related Financial Disclosures (the TCFD). Thus, this Climate and Nature Report has been developed to support our stakeholders in locating climate- and nature-related information contained in our Sustainability Report 2022 (including its Supplementary Information document).

For further pertinent documents, refer to ubs.com/gri

About this report

The reporting period for our Sustainability Report as well as our Climate and Nature Report is 1 January to 31 December 2022 which is aligned with the financial reporting period. All data included in the report is therefore for this period, unless otherwise indicated. Data pertaining to our firm’s own environmental footprint covers the reporting period 1 July 2021 to 30 June 2022. Data showing progress against our net-zero sectorial targets pertains to 31 Dec 2021 (due to the unavailability of relevant 2022 data, as explained in the respective section of this report).

Unless otherwise noted, the information included in this report is presented at the consolidated level for UBS Group AG and UBS AG. UBS Group AG and UBS AG consolidated information does not differ in any material respect. Supplementary information regarding certain significant subsidiaries can be found in “Note 28 Interests in subsidiaries and other entities” in our Annual Report 2022.

The purpose of this report is to support our stakeholders in locating climate- and nature-related information contained in our Sustainability Report (including its Supplementary Information document) in one document that follows the structure recommended by the Task Force on Climate-related Financial Disclosures (the TCFD). For this report, we also leveraged the beta framework of the Taskforce on Nature-related Financial Disclosures (released in November 2022). In addition to our Sustainability Report and Supplementary Information document, other information on sustainability topics, including our Sustainability Accounting Standards Board (SASB) index, our World Economic Forum International Business Council (WEF IBC) Stakeholder Capitalism Metrics reference table and our Principles for Responsible Banking (PRB) reporting and self-assessment are available from ubs.com/gri.

Explanation on dependencies

Certain activities of UBS that pertain to the implementation of its sustainability and impact strategy are directly impacted by factors that UBS cannot influence directly or can only influence in part. These include pertinent governmental actions (e.g., when it comes to the achievement of the Paris Agreement and thus the achievement of our firm’s net-zero ambitions); the quality and availability of (standardized) data (e.g., in such areas as emissions); the development and enhancement of required methodologies and methodological tools (e.g., on climate- and nature-related risks); the ongoing evolution of relevant definitions (e.g., sustainable finance); or the furthering of transparency (e.g., pertaining to company disclosures of data). Areas where these dependencies are of particular relevance (including in particular regarding the examples noted above) are explained in the relevant sections of our Sustainability Report and our Climate and Nature Report.

6 March 2023

UBS Group AG and UBS AG

Contacts

Our Corporate Responsibility team, part of the UBS Chief Sustainability Office, manages UBS’s sustainability disclosure and provides information to stakeholders about the content of this report.

cr@ubs.com

Governance

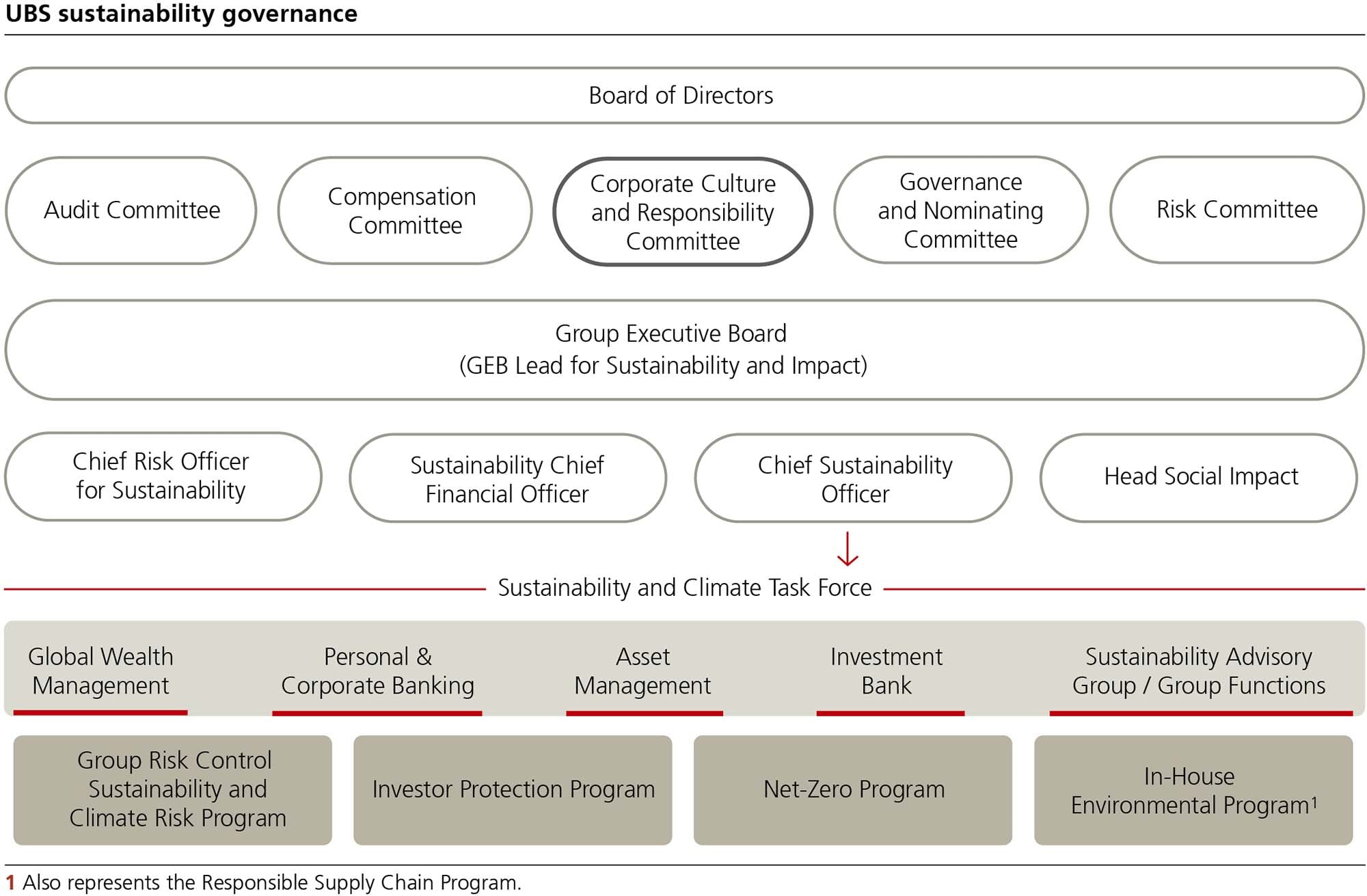

Our sustainability governance

Board of Directors and Group Executive Board

Our firm’s sustainability and corporate culture activities are grounded in our Principles and Behaviors and overseen at the highest level of the organization. These principles are laid down in our Code of Conduct and Ethics.

Our Board of Directors has ultimate responsibility for the strategy and the success of the Group and for delivering sustainable shareholder value. It oversees the overall direction, supervision and control of the Group and its management. It also supervises compliance with applicable laws, rules and regulations.

Five committees support the Board of Directors of UBS Group AG (the BoD) in fulfilling its duty through the respective responsibilities and authority given to them. All BoD committees have specific responsibilities pertaining to environmental, social and governance (ESG) matters, e.g., the Compensation Committee is responsible for ESG-related compensation topics, the Risk Committee supervises the integration of ESG in risk management, the Governance and Nominating Committee supports the Board in establishing best practices in corporate governance and the Audit Committee has oversight of the control framework underpinning ESG metrics.

Our BoD’s Corporate Culture and Responsibility Committee (the CCRC) is the body primarily responsible for corporate culture, responsibility and sustainability.

The CCRC oversees our Group-wide sustainability and impact strategy and key activities across environmental and social topics, including climate, nature and human rights. Annually, it considers and approves our firm’s sustainability and impact objectives.

Our Group Executive Board (the GEB) develops the strategy for the Group. It is responsible for managing our assets and liabilities in line with the Group’s strategy, regulatory commitments and the interests of our stakeholders. As determined by the BoD’s Risk Committee, the GEB manages the risk profile of the Group as a whole. It has overall responsibility for establishing and implementing risk management and control in our firm. The responsibility for setting the sustainability and impact strategy and developing Group-wide sustainability and impact objectives, in agreement with fellow GEB members, has been delegated to the GEB Lead for Sustainability and Impact by the Group chief executive officer (the Group CEO). Progress against strategy and the associated targets are reviewed at least once a year by the GEB and the CCRC.

Our GEB Lead for Sustainability and Impact manages the Group Sustainability and Impact (GSI) organization and, together with our Chief Sustainability Officer (the CSO), co-chairs the Sustainability and Climate Task Force (the SCTF). Both our GEB Lead for Sustainability and Impact and our CSO are also permanent guests of the CCRC.

Group Sustainability and Impact

GSI consists of the Chief Sustainability Office and the Social Impact Office, headed by the CSO and Head Social Impact, respectively. The CSO is responsible for driving the implementation of the Group-wide sustainability and impact strategy, including reporting on our progress toward net zero (and the execution thereof by our business divisions and Group Functions).

The Head Social Impact is responsible for driving and implementing the Social Impact strategy, including Community Impact, Philanthropy Services and UBS Global Visionaries. Reporting to the Head Social Impact, the regional Heads of Social Impact and Philanthropy are responsible for extending the reach of and maximizing the impact of our social impact activities locally, nationally and globally. In addition, they have responsibility for all our programs’ operations and risk management, client engagement, and employee volunteering.

Progress made in implementing Group-wide sustainability and impact objectives is reported as part of UBS’s annual reporting. This reporting is reviewed and assured externally according to the requirements of the Sustainability Reporting Standards of the Global Reporting Initiative (the GRI Standards). UBS is certified according to ISO 14001.

Refer to the “Appendix 1 – Governance” section of this report for additional information on our sustainability governanceThe Sustainability and Climate Task Force

The Sustainability and Climate Task Force (the SCTF) is the authority for divisional and functional sustainability and climate governance, as well as the Group’s sustainability and climate governance. The SCTF’s role includes the approval of the actions required to achieve our firm’s climate strategy, monitoring progress against that strategy and providing assurances to the GEB that UBS manages climate risk and opportunities in a proper manner.

Firm-wide sustainability groups

The Sustainable Finance Group

The Sustainable Finance Group (the SFG) is chaired by the CSO and supports the implementation of the sustainability and impact strategy as it relates to sustainable finance across the firm.

The Sustainability Advisory Group

The Sustainability Advisory Group (the SAG) is chaired by the CSO and is organized by the SAG’s convener, who has a reporting line to the CSO. It provides a mechanism for disseminating and cascading relevant information regarding Group-wide sustainability and impact efforts into UBS’s various control and aligned functions.

Governance of key areas

Sustainability and climate risk

Our management of sustainability and climate risk (SCR) is steered at the GEB level. Reporting to the Group CEO, the Group Chief Risk Officer is responsible for the development and implementation of control principles and an appropriate independent control framework for SCR within UBS, together with its integration into the firm’s overall risk management and risk appetite frameworks. Our SCR Policy Framework is applied Group-wide to relevant activities, including client and supplier relationships.

Refer to the “Appendix 3 – Risk management” section of this report for more details about our SCR Policy FrameworkThe Sustainability Chief Financial Officer

Our Sustainability Chief Financial Officer (SCFO) supports the new and expanding requirements that are being driven by our global sustainability agenda. With reporting lines both to the Group Chief Financial Officer (GCFO) and to the GEB lead for Sustainability and Impact, the SCFO works closely with the Group Controller and Chief Accounting Officer’s team and is the primary lead on sustainability topics for the GCFO. The SCFO ensures that sustainability considerations are embedded into our financial decision-making processes, supports the expanding external sustainability disclosures arising from both new regulatory requirements and voluntary commitments made by our firm, and ensures the continued development of the financial control environment that underpins our disclosures.

The Net-Zero Program

The Net-Zero Program (the NZP) coordinates implementation of the commitments set out in our “Net Zero and Beyond” statement, with a specific focus on reducing emissions related to our financing activities. The NZP reports into the SCTF and includes members from various Group functions and those teams that support our clients with financing.

The Investor Protection Program

The Investor Protection Program coordinates the implementation of several sustainability-related regulations of the European Union, the European Economic Area, the UK, Switzerland, Singapore, the Hong Kong SAR and the US, as well as related parts around UBS’s own commitments, in the context of client investments. The regulations are designed to provide clients with transparency and comparability of sustainable investment products, helping them align investments with their sustainability objectives. They require the integration of ESG metrics into our investment portfolio and risk management processes, as well as reporting to clients and regulators.

In-house environmental management

Our in-house environmental management is steered by the Chief Digital and Information Office (the CDIO). Reporting to the Group CEO, the CDIO is responsible for driving the reduction of the environmental impact from our offices, our technology and our supply chain. The CDIO implements the sustainability and impact strategy within UBS’s operations by ensuring local legal compliance, monitoring and measuring of environmental and energy performance, and continuous improvement according to ISO 14001, the international environmental management standard, and ISO 50001 (Region EMEA).

Nature

Our approach to nature is overseen by the BoD, in particular by the CCRC, as part of its responsibility for sustainability topics. In 2022, the CCRC received its first dedicated update on nature and biodiversity, including the progress of the Taskforce on Nature-related Financial Disclosures (the TNFD) and UBS’s own activities relating to the TNFD. We expect these updates to continue annually.

The GEB is responsible for driving our nature-related efforts, as part of its sustainability and impact activities. GSI then coordinates these efforts and provides periodic updates to the GEB through GSI strategy management reports. The business divisions and Group Functions ensure the implementation of UBS’s nature-related strategy and risk management frameworks.

Controlling risks and metrics

GCRG Sustainability Expert Group

Our Group Compliance, Regulatory & Governance (GCRG) function is responsible for the ongoing monitoring of the adequacy of our control environment for non-financial risks (NFR) and sets out requirements for the design and operation of 1st LoD (Line of Defense) and 2nd LoD controls across Operational Risk, Compliance and Financial Crime Prevention. GCRG is actively engaged across UBS’s Risk Committee structure and supervisory board governance. It drives the review and, where necessary, the required adaptations to our NFR frameworks to align the independent control and oversight capabilities with existing and new regulations and changes across business activities.

In 2022, GCRG established the Sustainability Expert Group (the SEG, with senior representatives from across the divisional, regional and functional GCRG units, supported by senior experts across Group Legal, Group Risk Control, Sustainability CFO and Group Sustainability and Impact. In 2022, we focused our activities on initiating a range of enhancements to our ESG NFR risk assessment and process control coverage whilst undertaking appropriate reviews of the integration of ESG factors into the NFR control framework. This included considerations relevant to the consistent assessment, monitoring and escalation of high inherent reputational risk – incorporating ESG factors.

In this context GCRG maintains a quarterly dynamic ESG NFR Assessment, which acts as both the basis for its global view on ESG NFR in UBS, as well as a key input for the decision-making for the SEG priorities and associated risk reviews. We performed multiple ESG-related NFR assessments, focusing in particular on the effectiveness of processes and controls designed to mitigate greenwashing risk. This included reviews of relevant framework elements such as reputational risk, as well as specific deep-dives into product lifecycle management across the business divisions, including marketing material and product disclosure. With regards to control coverage more specifically, GCRG also enhanced core global controls relating to new business initiatives, client onboarding and oversight of marketing materials related to sustainability, and integrated ESG topics into the standard regulatory change event process for firm-wide coverage.

Refer to “Non-financial risk” in the “Risk management and control” section of our Annual Report 2022 for more informationSustainable Finance Legal

Global Sustainable Finance Center of Legal Excellence, a part of our Group Legal division, provides legal and strategic advice on sustainability-related matters to the GEB sponsor for sustainability and impact, the Chief Sustainability Office, the business divisions, and other group functions. The team works closely with lawyers supporting the business divisions and Group Functions.

Strategy

Our sustainability and impact strategy

What climate and nature mean to us

Finance has a powerful influence on the world. At UBS we reimagine the power of people and capital, to create a better world for everyone: a fairer society, a more prosperous economy and a healthier environment. That is why we partner with our clients to help them mobilize their capital toward a more sustainable world and why we have put sustainability at the heart of our purpose.

Our ambition

We want to be the financial provider of choice for clients that wish to mobilize capital toward the achievement of the United Nations’ 17 Sustainable Development Goals (the SDGs) and the orderly transition to a low-carbon economy.i We are focusing on three key areas to drive that transition: Planet, People and Partnerships. In the following we focus on the first key area, planet.

Planet first

Reaching net zero is an ambitious goal, but we are committed to doing our part. The shift toward a lower-carbon future is a priority for UBS and it is a key focus of our sustainability strategy.

We have set aspirational goals to achieve net-zero greenhouse gas (GHG) emissions from our own business and we are directing capital toward the low-carbon transition by offering the choice our clients need to effect the change that they want to see. At the same time, we are focused on managing the risks related to climate, natural capital and biodiversity to protect our clients’ assets and those of our firm from the impact of climate change. We are also seizing the opportunities from the low-carbon transition.

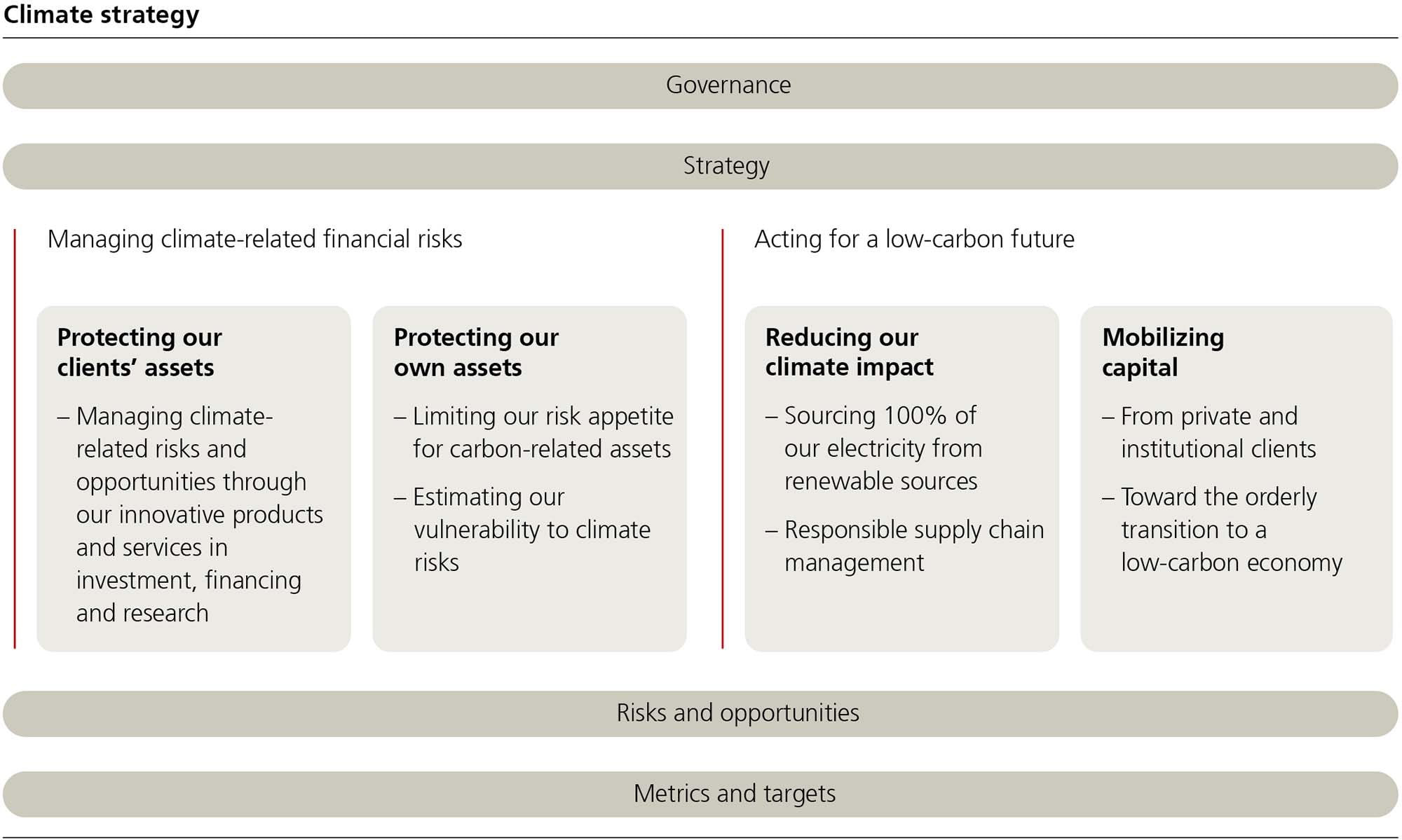

Our climate strategy is a reflection of our focus areas and covers two main areas: managing climate-related financial risks, and taking action on a net-zero future, via four strategic pillars:

Climate strategy

Our climate strategy covers two main areas: managing climate-related financial risks and taking action on a net-zero future. Underpinning these two main areas are four strategic pillars:

1. Protecting our clients’ assets

As a global financial institution, it is our responsibility to help clients navigate through the challenges of the transition to a low-carbon economy. We help our clients assess, manage and protect their assets from climate-related risks by offering innovative products and services in investment, financing and research.

We work collaboratively across our industry and with our clients, ensuring they have access to best practice, robust science-based approaches, standardized methodologies and quality data for measuring and mitigating climate risks. Our activities include engaging on climate topics with the companies we invest in. For example, our Asset Management business division has implemented an engagement program with companies from the following sectors: oil and gas, electricity and other utilities, metals and mining, construction materials, chemicals, and automotive. During 2022, we also voted upon climate-related resolutions at 160 companies.

As part of our commitment to implementing the recommendations of the Task Force on Climate-related Financial Disclosures (the TCFD), we also strive to integrate these recommendations into our decision-making and processes pertaining to services, strategies or products offered or employed by third parties, including delegates.

2. Protecting our own assets

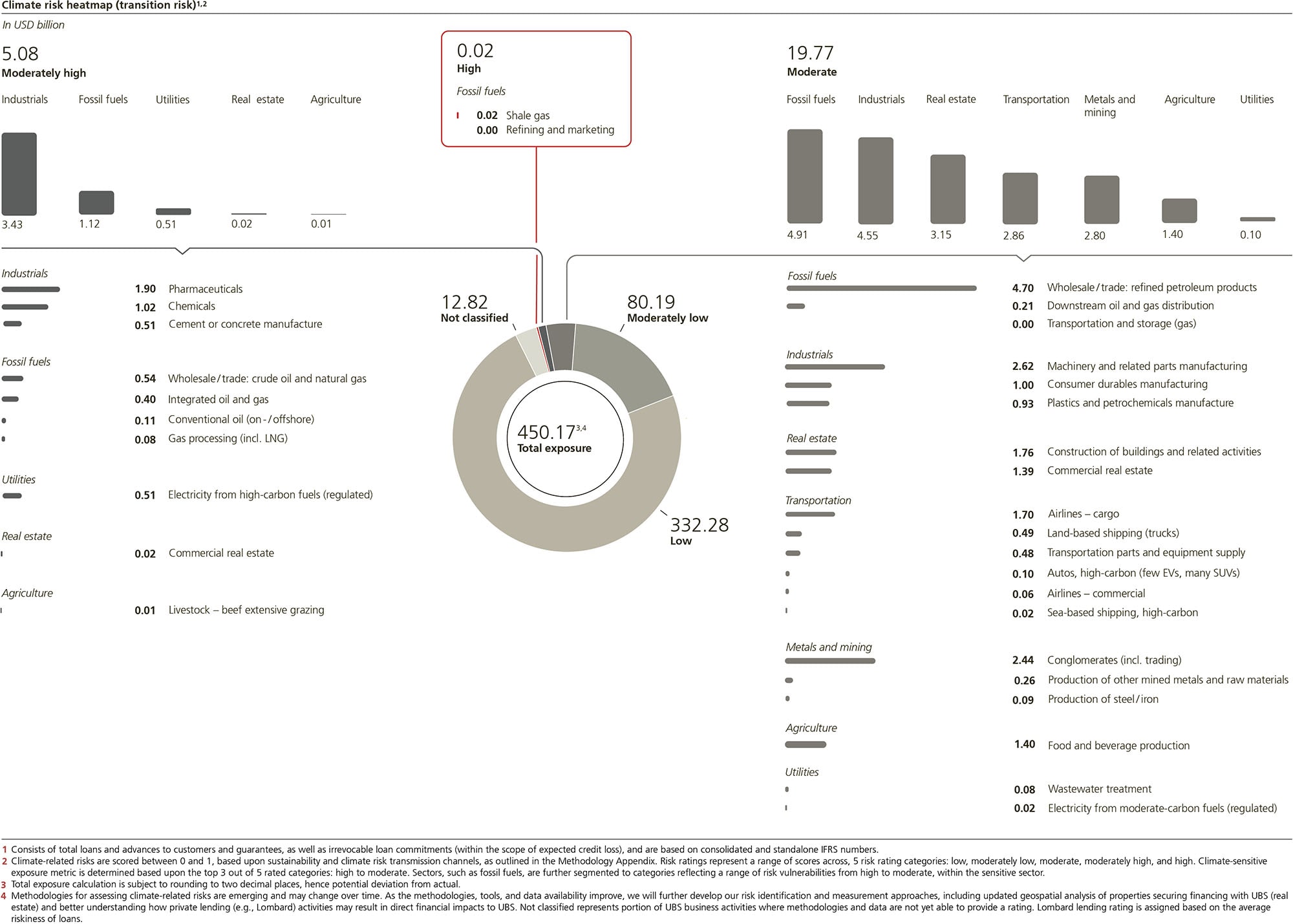

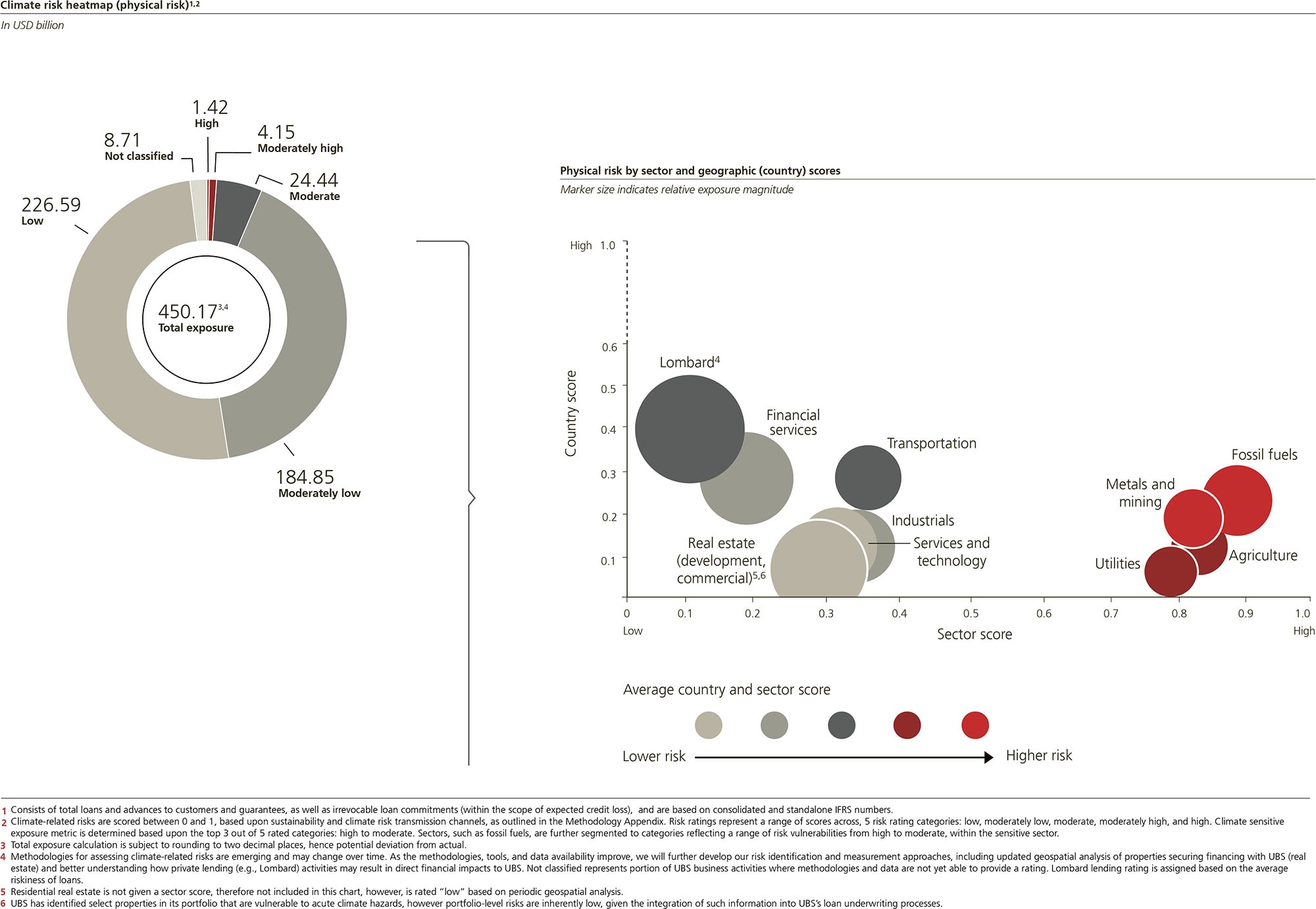

We seek to protect our assets by limiting our risk appetite for carbon-related assets. We use scenario-based stress testing approaches and other forward-looking portfolio analyses to estimate our vulnerability to climate-related risks. As of 31 December 2022, we had reduced our lending exposure to carbon-related assets to 7.5% (USD 33.8 billion) of our total customer lending exposure. This is down from 8.0% at the end of 2021 and 8.6% at the end of 2020.

Carbon-related assets are defined as significant concentrations of credit exposure to assets tied to the four non-financial groups as defined by the TCFD (using the Global Industry Classification Standard, the GICS). These four groups are (i) energy; (ii) transportation; (iii) materials and buildings; and (iv) agriculture, food and forest products. Recognizing that the term carbon-related assets is currently not well defined, the TCFD encourages banks to use a consistent definition to support comparability. We continue to collaborate with the industry to drive further consistency.

3. Reducing our climate impact

We are committed to achieving net-zero emissions in our own operations (scopes 1 and 2) by 2025. We will do this by replacing fossil fuel heating systems, while striving 100% renewable electricity coverage and investing in credible carbon removal projects (including negative emissions technology). We are compensating for our historical scope 1 and 2 emissions back to the year 2000 and have sourced credible and clear carbon offsets and investments in nature-based solutions. As standards in this area continue to evolve (e.g., the Core Carbon Principles from the Integrity Council for Voluntary Carbon Markets), we will seek to apply them to our activities. Furthermore, we are currently working to understand and quantify the scope 3 emissions in our supply chain. We are engaging with our key vendors about targeting net zero by 2035.

4. Mobilizing capital

We mobilize private and institutional capital through investments that help the world mitigate and adapt to climate change.

We were the first major global financial institution to make sustainable investments the preferred solution for our private clients wishing to invest globally. We also support our goal of mobilizing capital as a lender and as an arranger, underwriter and/or structurer of securities. For corporate clients, we support the issuance of green, social, sustainability and sustainability-linked bonds, as well as the raising of capital in international capital markets, in line with recognized market guidelines, such as the ICMA Green Bond Principles and, in relation to green and sustainable loans, the Loan Market Association (LMA) Green Loan Principles and the LMA Sustainability-linked Loan Principles.

Detailed data accounting of our financed emissions helps us identify climate-related opportunities requiring capital, and improve and tailor our sustainable product range for clients. Additionally, such insights help UBS, our partners and our clients in a number of ways. For instance, they reduce the risk of stranded assets.

Green Funding Framework

Our Group-wide Green Funding Framework sets out how we intend to connect our sustainability objectives with access to financial markets through a variety of funding products.

Refer to ubs.com/greenbonds for more details about the Green Funding Framework, external reviews and annual reporting (including impact and allocation reporting)Our approach to nature

We manage risks and opportunities related to natural capital and biodiversity across our activities, in line with our commitment to mobilize capital toward the achievement of the SDGs and our participation in the Taskforce on Nature-related Financial Disclosures (TNFD). During 2022, we also supported the establishment of a Swiss TNFD national consultation group to support capacity building in our home market.

We recognize the challenges of transitioning toward a society that can meet both human needs while living within the constraints of natural resources, with the objective of also generating net positive outcomes for our natural environment. These challenges are reflected in stark numbers: for example, the World Economic Forum (WEF) estimates that about USD 44 trillion worth of economic value depends on the natural world in some way while a recent UNEP report states that flows to nature-based solutions are currently USD 154 billion per year, less than half of the USD 384 billion needed by 2025. An assessment by Moody’s Investors Service puts almost USD 1.9 trillion at risk across nine sectors due to loss of biodiversity. The challenges also find expression in opportunities, with, e.g., the Paulson Institute valuing the market for biodiversity investments at a potential USD 93 billion by 2030 (up from some USD 4 billion in 2019).i We look forward to the setting of global policy objectives and goals through the Convention on Biological Diversity. Public policy has played and will continue to play a critical role in steering and incentivizing markets that will drive the transition to a sustainable economy.

Partnerships bring it together

The challenges our world faces cannot be solved by one organization alone. That is why we partner with other thought leaders and standard setters to unite around common goals that can drive change at a global scale.

Refer to the Sustainability Report’s Supplementary Information document for more about our partnerships and our approach to themDelivering our sustainability commitments and strategy

Integrating climate-related impacts in our financial planning

UBS operates a multi-year financial planning process. This process reflects our business position, corporate strategy and prospective economic environment. Sustainability is a core component of that strategy and planning process, with particular focus on net zero (scopes 1, 2 and 3), sustainability-related assets and investments and philanthropy.

The underlying drivers of our sustainability investments are also considered. These include our own corporate commitments, regulatory and other external requirements, and client-servicing opportunities. The changing global outlook regarding sustainability, and climate change in particular, is reflected in the process, with the risks associated with climate change being reflected in our capital requirement planning calculations.

Our corporate positioning, in terms of balance-sheet exposure and contractual duration, our risk management activities and the nature of the underlying risk, mean we do not currently view climate change as a material risk factor. However, formal guidance on capital-framework calculations is subject to ongoing market and regulatory discussion, and we will continue to reflect this in our planning processes.

Refer to our Annual Report 2022 for more information on UBS’s financial planning processSustainability in remuneration

Environmental, social and governance (ESG) objectives are considered in the compensation determination process in objective setting, performance award pool funding, performance evaluation and compensation decisions. ESG-related objectives have been embedded in our Pillars and Principles since they were established in 2011. In 2021, we introduced explicit sustainability objectives in the non-financial goal category of the Group CEO and GEB scorecards. These sustainability objectives are linked to our priorities, and their progress is measured via robust quantitative metrics and qualitative criteria. Sustainability objectives are individually assessed for each GEB member, and consequently directly impact their performance assessments and compensation decisions.

In addition, in the performance award pool funding across the Group, ESG is also reflected through an assessment of progress made against targets linked to our focus areas of Planet (including climate-related goals), People (including progress made against our diversity ambitions) and Partnerships, alongside other key dimensions. Therefore, ESG is taken into consideration when the Board of Directors’ Compensation Committee assesses not only what results were achieved but also how they were achieved. For 2022, we established robust and concrete targets, and made good progress toward achieving them. We continue to increase our focus on this topic.

Refer to “GEB performance assessments“ in our Compensation Report 2022 for more information Refer to “Our focus on sustainability and climate,” “Employees” and “Social impact” in our Annual Report 2022 for more information Refer to ubs.com/gri for more information about ESG-related topicsSustainability education

Our in-house UBS University delivers formal training, along with quick learning bites and other resources. Our largely online offering focuses on building skills for use now and in the future and includes specialized business training, client advisor certification and both leadership and line manager training. We introduced foundational training on sustainability and sustainable finance in 2022, and modules on agile working, data literacy, regulatory requirements, diversity and inclusion, well-being and other topics round out the curriculum. In 2022, our full-time employees completed more than 1,327,000 learning activities, for an average of two training days per employee.

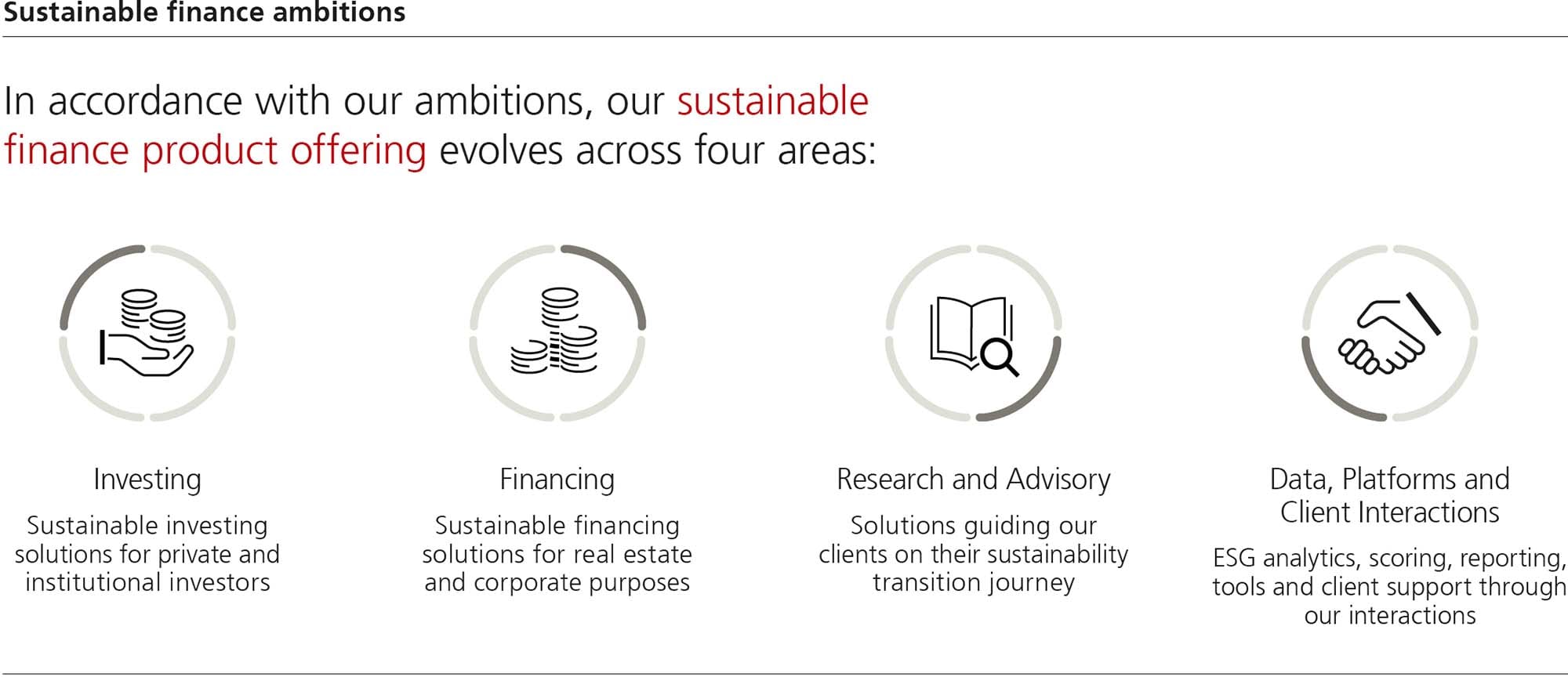

Refer to “Group Sustainability and Impact management indicators“ in the Sustainability Report’s Supplementary Information document for further information on relevant trainingsOur approach to sustainable finance

Supporting our clients

Sustainable finance is crucial when it comes to helping our clients achieve their diverse sustainability objectives. Through our product and service offering, we target four key objectives in serving our clients:

- The power of choice: We want to give our investing clients the choice they need to meet their sustainability objectives.

- A smooth transition: We aim to support our clients in their transition to a low-carbon economy, for instance, by offering innovative sustainable financing solutions.

- Safely managing risks and identifying opportunities: We offer research and insights, together with analytics services. Combined with targeted advice, they are designed to help clients mitigate their risks and spot new opportunities.

- Making sustainable finance an everyday topic: We want to make sustainability topics tangible throughout our interactions with clients. To help us do that, we provide support in the form of tools, platforms, and education.

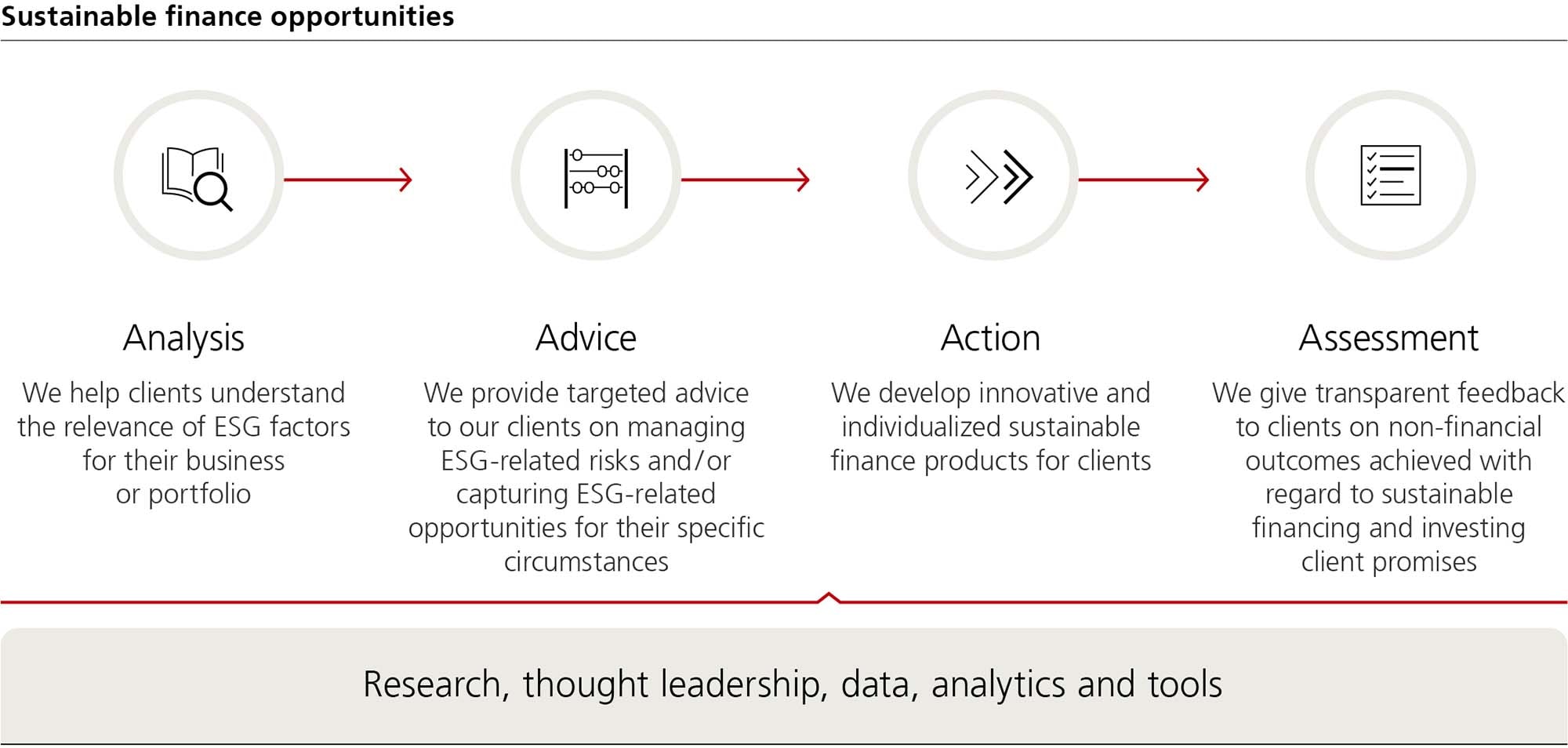

Identifying sustainable finance opportunities

Our Sustainable Finance Group (the SFG) brings together UBS’s senior sustainable finance experts and business leads. In view of our firm’s diversified business model, it has been established as a cross-divisional group. Chaired by our Chief Sustainability Officer, the SFG helps to identify strategic sustainability themes for the development of innovative products and services. It plays an important role in furthering internal collaboration, synergies, and consistency. For example, it acts as a steering body for initiatives that help drive commercial activities and outcomes. It also helps develop firm-wide sustainable finance product guidelines and leads the analysis of important market and financial industry trends.

Defining sustainable finance

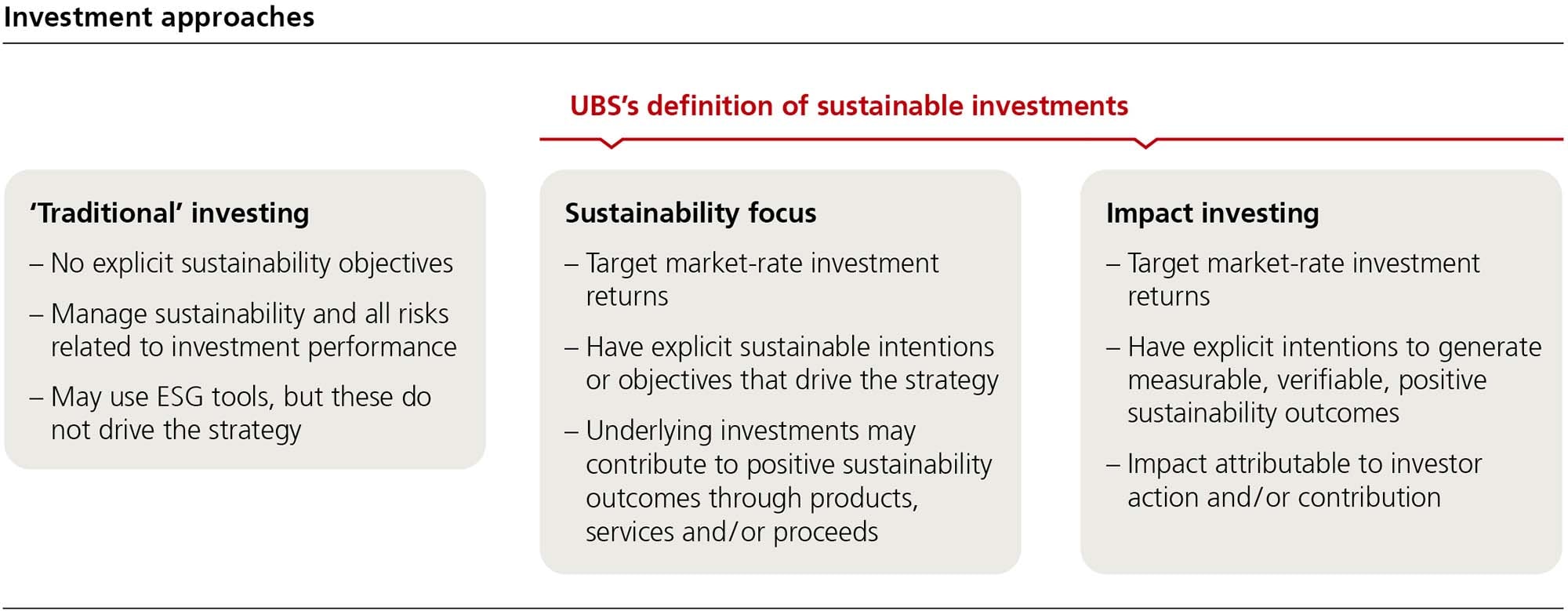

It is important to set out how we define sustainable finance (SF) as, at present, there is no global, uniformly accepted definition. SF comprises any financial product or service (including both investing and financing solutions) that aims to explicitly align with and/or contribute to sustainability-related objectives, while targeting market-rate financial returns. Sustainability-related objectives may include but are not limited to the Sustainable Development Goals identified in the United Nations' 2030 Agenda for Sustainable Development.

This definition is also reflected in our Group SI framework, which specifically defines “sustainability focus” and “impact investing” products. Both categories reflect a defined and explicit sustainability intention of the underlying investment strategy. This intentionality differentiates them from “traditional” investment products, or those that consider ESG aspects but do not actively and explicitly pursue any specific sustainability objective, such as ESG integration- or exclusions-only approaches.

Refer to the Sustainability Report’s Supplementary Information document for more on ESG integration and exclusion

Challenges and opportunities

2022 was a challenging year for our clients, with volatile financial markets, significant geo-political events and rising inflation across many economies. Our comprehensive offering of research and advisory products played an important role in helping our clients better understand these complex developments, as well as the implications for their portfolios and businesses.

Against the backdrop of global challenges, financial markets contracted across asset classes during 2022. For investments, global open-ended fund and ETFs total net assets decreased by 19%i in 2022. Despite this downturn, the long-term trajectory for sustainable investing remains one of growth, demonstrated by continuous quarterly inflows into sustainable investing products while “traditional,” non-SI products faced outflows throughout most of 2022.i In line with these global market developments, at UBS we continued to increase SI assets under management (AuM) as a share of total AuM, reaching 6.8% by the end of 2022, up from 5.5% at the end of 2021.

Financing markets were equally impacted by the difficult macro environment, where overall bond market issuances dropped by 21%.i This was reflected in the market for green, social, sustainability and sustainability-linked (GSSS) bonds, where global issuance dropped by 22%.i Despite these headwinds, we continued to increase our activity in the GSSS bond markets in EMEA, where UBS-involved GSSS bond issuance increased by 8% year on year.

We continued to maintain a dominant position in our fast-growing home market of Switzerland, securing leadership in the league table in the Swiss Franc market with a 44% market share.

Sustainable investing for our clients

In 2022, we made progress on a number of important investment product initiatives relevant to a broad spectrum of clients across our business areas. For example:

- We made it easier for private clients to access sustainable investment products and services, suited to their individual preferences, e.g., through expanded access to our Advice SI and separately managed account (SMA) solutions, and new targeted sustainability and impact offerings. In line with EU regulations for clients in scope, UBS systematically captures clients’ preferences when it comes to SI.

- We expanded the range of sustainability and impact funds in public and private markets and exchange-traded funds (ETFs) available to private, institutional, and corporate clients.

- We continued to provide customized, tailored, and structured investment solutions for private and institutional investors.

Launching innovative sustainable investing products

Transition and impact are key focus areas for our clients and the financial industry in general. In response, we launched several dedicated investment strategies supporting the allocation of capital to thematic areas such as decarbonization or energy storage.

SI solutions for private clients – addressing individual preferences

- Private market impact vehicles: We made available six private market funds providing investment opportunities aligned with the SDGs available to clients.

- Personalized Sustainable Investing (PSI) SMAs: Launched by our Global Wealth Management business division in the US, managed by our Asset Management teams and powered by our Chief Investment Office (CIO), it addresses demand for customization by allowing clients to personalize specific strategies to align with their individual sustainability preferences.

- Inclusive Investing: Launched by Global Wealth Management in the US, the offering aims to address investor preferences for strategies that support diversity, equity and inclusion and amplify the CIO longer-term investment theme on diversity and equality. Over time, the focus will be on enhancing capabilities and educating financial advisors and clients on the offering.

- Sustainability-focused hedge fund: Our advisory clients can benefit from an expanding platform of alternative SI products. In 2022, we have onboarded a hedge fund aiming to invest in sustainability themes and short businesses facing potential disruption from sustainability-related trends.

- Future of Earth fund: Launched in 2021, this fund promotes environmental objectives built around the themes of sustainable land use, sustainable water use, the shift to clean energy and providing health solutions that may help mitigate the impacts of environmental degradation on human health.

Customization for institutional investing clients

- Aon Transition and SDG fund: We joined forces with Aon in March 2022 to co-develop and launch the UBS Global Equity Climate Transition Fund. The Aon MasterTrust and Group Personal Pension Plan seeded the fund with more than GBP 700 million. This collaboration brings together our award-winning proprietary Climate Aware Framework and our global stewardship program to help companies such as Aon transition towards a lower-carbon future while also meeting their broader sustainability preferences.

- Innovation fund: We launched this fund in August 2022 to invest in leaders across four key areas: planet / climate, people / health, digitalization and additional diversifiers. We know these issues are continually evolving. Some of the sleeves provide exposure to important sustainability themes and high conviction strategies. One example is the UBS Healthy Living strategy, a mix of established companies with long-term experience in healthy living, and fast-growing market players.

- Energy storage: Our Asset Management business division acquired five standalone, development-stage energy storage projects in Texas from Black Mountain Energy Storage (BMES). This acquisition forms part of the strategic expansion of Asset Management’s infrastructure business, providing clients with further sustainable investing opportunities in the alternatives space. It marks an important milestone following the establishment of the Energy Storage Infrastructure team in 2021. The projects will provide flexibility, responsiveness and dispatchability to the Electric Reliability Council of Texas (ERCOT) grid once it becomes operational in 2024. These capabilities make energy storage a critical component of grid reliability and a key technology for the energy transition, helping ERCOT and the Texas consumers it serves benefit from innovation and more economic sources of energy.

- UK life sciences fund: We raised GBP 400 million in the first closing of a UK life sciences fund which aims to develop research and development and advanced manufacturing facilities for the sector in the UK. These facilities are required in order to facilitate the growth of life sciences and the advancement of novel healthcare products. They also create significant skilled employment opportunities for local economies and population.

- Transition fund: We collaborated with Essex Pension Fund and Hymans Robertson to launch an investment fund specifically tailored to meet Essex Pension Fund’s objectives to invest in companies leading the transition to a low-carbon economy. In addition, the investment fund makes a positive social contribution by favoring companies that align with five of the SDGs.

Structured products and solutions for institutional and private clients

- Carbon emissions: Our clients continued to allocate to solutions linked to the recently launched UBS CMCI (Constant Maturity Commodity Index) Emissions Index or carbon emissions futures directly.

- Bespoke ESG portfolio: Bespoke investment methodology offerings with a custom ESG screening and a climate change focus.

- Actively Managed Certificates: Portfolio certificates linked to a range of sustainability and climate investment themes actively managed by private banks.

Actively driving the sustainability transition in Asset Management

We believe active ownership has an important role to play in helping to drive the sustainability transition. So, we engage with companies, issuers and standard setters to help make a demonstrable contribution to portfolios and sustainability outcomes. Collaboration with like-minded investors, as well as our ongoing partnership with clients, are key to achieving impact on a global scale.

- Climate opportunities: We joined the Energy Storage Solutions Consortium to pioneer methods of assessing and maximizing the greenhouse gas emissions benefits of stored energy usage. The goal is to create an open-source, third party-verified methodology to quantify the emissions benefits of certain energy storage projects and provide guidance on maximum emissions reduction benefits through stored energy.

- Stewardship: In our voting at annual shareholder meetings we require, as of 2022, 30% gender diversity at board level for large cap companies in developed markets, including markets generally lagging in this regard, such as Japan. In addition, we withheld support for the election of board directors responsible for the nomination process at 441 Japanese companies (up from 204 in 2021), 49 Swiss (up from 25 in 2021), and 389 US companies (up from 32 in 2021) due to lack of gender diversity.

- Thematic engagement: Through our dedicated program, we engaged with companies on climate change, for the fourth year running. During this time, we have raised our expectations for companies significantly, including enhanced disclosure of climate risks, and a greater focus on decarbonization ambitions and actions companies are taking towards a net-zero future. We continue to use collaborative engagement as a lever to scale our impact, in addition to our direct engagement, through our membership of Climate Action 100+. As of end of 2022, via Climate Action 100+, we co-led on five company engagements and participated in 20 company engagements. We are also a member of the FAIRR (Farm Animal Investment Risk and Return) initiative, the largest investor collaboration focused on ESG risks in the food and agriculture sector, we engage as the lead every year with one of the 25 companies targeted via the “sustainable protein engagement” program. Through engagement on sustainable proteins, we aim to reduce negative externalities from traditional protein production.

Leading by example

In 2022, our Group Treasury continued to invest its high-quality liquid assets (HQLA) portfolios under a dedicated Treasury ESG Investment Framework, which integrates ESG considerations in the investment process alongside more traditional economic and risk dimensions. It supports investments in ESG-labelled securities that have a direct link to sustainable projects. More holistically, it promotes investments in issuers with positive ESG characteristics and flags potential risks. At year-end 2022, Group Treasury held more than USD 6.7 billion of green, social and sustainability bonds in its HQLA portfolios, a growth of 97% year on year, in contrast to declining global ESG bond issuance in 2022.

Financing a sustainable future

We develop financing solutions to help our clients transition to a more sustainable future. These solutions can be on-balance sheet (e.g., green or sustainable loans and mortgages) or off-balance sheet (such as access to debt and equity capital markets), and also included transaction structuring.

Our Investment Bank facilitated USD 48 billion of GSSS bonds financing through 77 bond deals for our clients, with a market-leading share of the Swiss franc GSSS bond market. Among our most notable transactions during 2022 were a UK Debt Management Office (DMO) Green Gilt transaction, as well as an inaugural green bond issuance for New Zealand Debt Management. In addition, UBS was the sustainability structuring advisor for the Republic of Philippines’ inaugural sustainability bond. These were pivotal for financing part of the respective governments’ plans for tackling climate change and other environmental challenges. They also funded much-needed infrastructure investment and created green jobs.

In our Swiss home market, we have been developing new and innovative real estate financing solutions to support our clients in the transition to a low-carbon economy. Key examples include:

- UBS Mortgage Energy for private clients: i We launched this offering to encourage clients to invest in more sustainable energy and heating systems, such as through replacing fossil fuel heating with a more sustainable alternative or by installing a photovoltaic system. In doing so, clients benefit from attractive interest rates and lower long-term energy costs.

- UBS Loan Energy for energy-efficient investment properties:i Our clients benefit from attractive interest rates and comprehensive advice for their low-energy properties. In addition, they can discuss sustainability matters with a Switzerland-wide network of real estate experts.

- For our financing clients we also include considerations of nature alongside other topics. Transition finance, for example, can be part of a broader process over time with the conclusion only evident years after the financing was provided. Nature can be built into transition finance transactions, particularly those that impact the physical environment.

- Nant de Drance power station: Inaugurated in September 2022, UBS contributed to the development of his innovative “water battery”, designed to help balance the renewable electricity grid not only in Switzerland but also Europe. Nant de Drance has 900 MW of power-generating capacity, equivalent to that of the Gösgen nuclear power plant in Switzerland. This innovative structure took nearly 14 years to build and UBS was part of several bond financings needed to provide the financial support for its construction. One of the priorities in the construction of Nant de Drance, as agreed with the licensing authorities, was reducing its environmental impact. Fifteen projects, at a total cost of CHF 22 million, have been, or will be, completed to offset the environmental impact of the construction of the pumped storage power plant and very high-voltage lines connecting the power plant to the power grid. Most of the projects aim to recreate specific biotopes locally, especially wetlands, in order to encourage recolonization of the area by certain rare or endangered animal and plant species in Switzerland.

Driving the debate

In a year of fundamental change, our priority has continued to be providing our clients with timely and targeted ESG content, strategic insights and advice. Through these we also aim to raise awareness, distil inherent complexities and further the debate around key sustainability topics as they grow in importance in the collective consciousness of companies, clients and the broader public. We deliver our views and insights through a variety of channels, including our dedicated research and advisory services for corporate clients, institutions and private clients, as well as our specialist sales teams. In addition to focused ESG research, we also provide sustainability-related thought leadership and insights at industry conferences and through broader thematic publications.

ESG content and research

We address the question most frequently addressed to our sell side research team of how ESG factors connect to the markets, sectors and companies under coverage in a number of ways:

- We flag ESG-relevant content with our ESG icon. In 2022, the number of reports carrying the icon rose by 50%. Our flagship ESG content is the ESG Radar series, developed in collaboration with sector analysts over years. By the end of 2022, UBS sector analysts had lead-authored a cumulative total of over 90 ESG Sector Radars. In July 2022, we launched the ESG Company Radar series (over 30 published by year end).

- We explore debates of interest to our clients through thematic and cross-sectoral collaborations.

- In 2022 we gained global depth through an expansion of the team, now present in London, New York, Hong Kong, Tokyo and Sydney.

- Some of the research pieces which resonated most with institutional clients in 2022 included “Global Sustainability: Inflation Reduction Act,” “EU Sustainability Regulation: It’s Complicated,” “State of the Global Energy Transition 2022,” and “Future of Food: Have plant-based protein sales peaked?”.

Our CIO continues to provide guidance to private clients on incorporating sustainability into investments, particularly in a diversified portfolio context. Our research and investment views, together with a differentiated sustainable investing asset allocation, enable clients to gain exposure to diversified cross-asset portfolios using building blocks with explicit sustainability objectives. In 2022, CIO expanded its guidance to include hedge funds and structured products, which enabled Global Wealth Management to expand its sustainable investing offering. We also provided clients with timely guidance on other topics including “Sustainable Investing in an Energy Crisis” and the “Renaissance of Nuclear Energy.”

CIO also continued to provide actionable investment ideas to clients via its monthly Sustainable Investing Perspectives publication and podcast series, complementing its quarterly Sustainable InSIghts report series which provides regular updates on the state of the SI market, a running list of answers to frequently asked questions, and educational content on making sense of ESG data and scores.

ESG Advisory

Our Global ESG Advisory team in Global Banking provides strategic advisory and capital-raising services by specifically accounting for the structural shift in investor preferences towards ESG investment opportunities. To do so, we have been building the capabilities to assess a corporate’s sustainability profile and to link that profile to ESG investor demand. We expect this approach to underpin all Global Banking transactions over time.

In 2022, we developed tools to aid corporate clients in their ESG profiling, such as ESG key performance indicator (KPI) benchmarking analysis, ESG ratings interpretation and ESG valuation levers, amongst others. In addition, we implemented internal tracking systems for our senior bankers to record ESG-related client interactions. This tracking aims to capture the progress we are making with clients in integrating ESG considerations into all aspects of our services. These interactions can range from discussions around ESG regulatory developments to ESG–focused strategic opportunities in mergers & acquisitions (M&A).

Thought leadership

Our UBS Sustainability & Impact Institute (SII) has brought together a collective of sustainability thought leaders from across UBS to engage on current and future topics. Over 2022, the SII gathered their insights and published white papers, opening up key topics such as systems thinking and natural capital (e.g., From Ozone to Oxygen), and decarbonization for wider discussion.

Progressing with data, platforms and analytics

We regard the availability of good data, analytics and technology capabilities as essential enablers for getting us to a more sustainable future. They will equally help our clients make informed sustainability-related investing and financing decisions. Through various entities, we offer solutions such as portfolio analytics, ESG scoring and reporting or design and development of platforms providing innovative ways to access markets.

How we helped our clients in 2022

- esg2go: We became a partner and member of the strategic committee of esg2go, which provides small- and medium-sized enterprises (SMEs) with detailed insights into their sustainability performance, based on ESG criteria. This takes the form of a sustainability rating score for the SME and an accompanying report which the SME can pass on to its stakeholders.

- UBS key4 banking app: We provide a digital banking offering, which includes a sustainable savings account alongside a conventional personal account. Furthermore, for every UBS key4 banking account opened, UBS offsets 100 kg of CO2 emissions with a donation to myclimate.

- key4 by UBS Green Mortgage (for self-occupied real estate): Our key4 by UBS mortgage platform allows investors to offer preferential mortgage terms if clients can demonstrate, via a certificate (e.g., Minergie), that the property they wish to finance meets certain environmental standards. This offer is targeted at private clients.

- key4 by UBS Energy Check: In collaboration with experts from pom+, a real estate consulting company with proven expertise in sustainable properties, key4 by UBS is offering a free energy check to determine the potential energy and cost savings of an investment property. Interested prospects or customers can use the tool to receive a concrete plan of action. A key4 client advisor will then discuss the results with them.

- UBS Sustainability Analytics: We support our Asset Servicing clients with this enhanced online tool to actively monitor, manage and improve the sustainability profile of their investment portfolios. The analysis provides insights on sustainability ratings, business activity checks and carbon emissions, and helps to reduce the carbon footprint of their portfolios and align it to their chosen climate glidepath.

- Carbonplace: We co-founded Carbonplace, a technology platform for the voluntary carbon market that has the goal of creating a streamlined and transparent market for our clients. We have been working collaboratively to help deliver on this initiative and launched two pilot transactions in 2022.

Taking action on a net-zero future

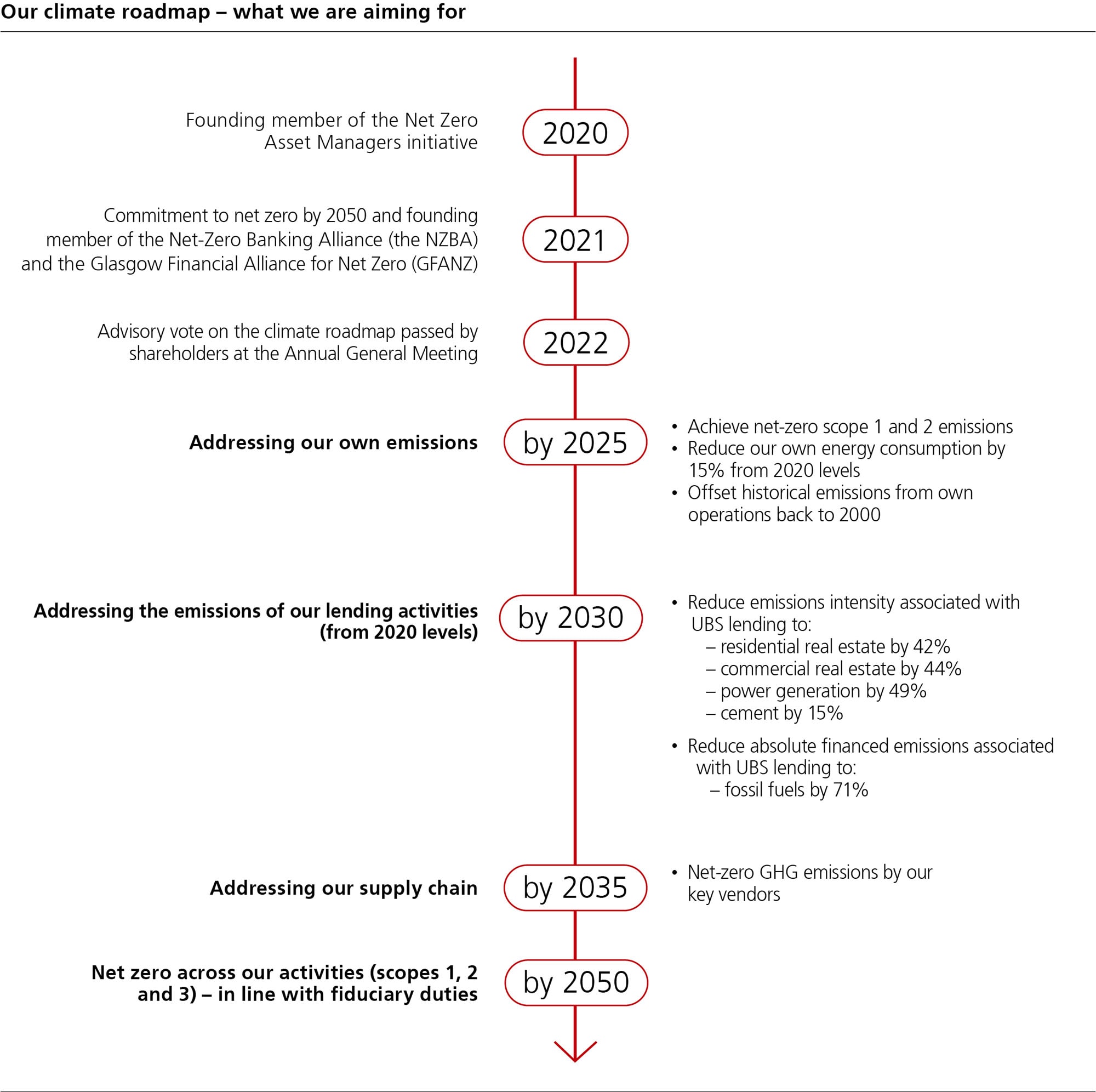

We recognize the vital importance of taking action to support the transition to a low-carbon economy. By 2050, we are aiming to achieve net-zero greenhouse gas (GHG) emissions for scopes 1, 2 and 3 across our business, in line with fiduciary duties. Our climate roadmap sets out how we aim to get there. It comprises three key aspects:

- net zero to reduce our direct climate impact;

- net zero to support the transition of our financing clients; and

- net zero to support the transition of the assets of our investing clients.

We are committed to standing with our clients to help them achieve their net-zero goals and to support the work governments around the world are doing to move the real economy to align with the Paris Agreement 1.5°C commitment. In Switzerland, where our firm has its headquarters, we look forward to partnering with regulators to identify appropriate goals for financial institutions under the country’s CO2-Act.

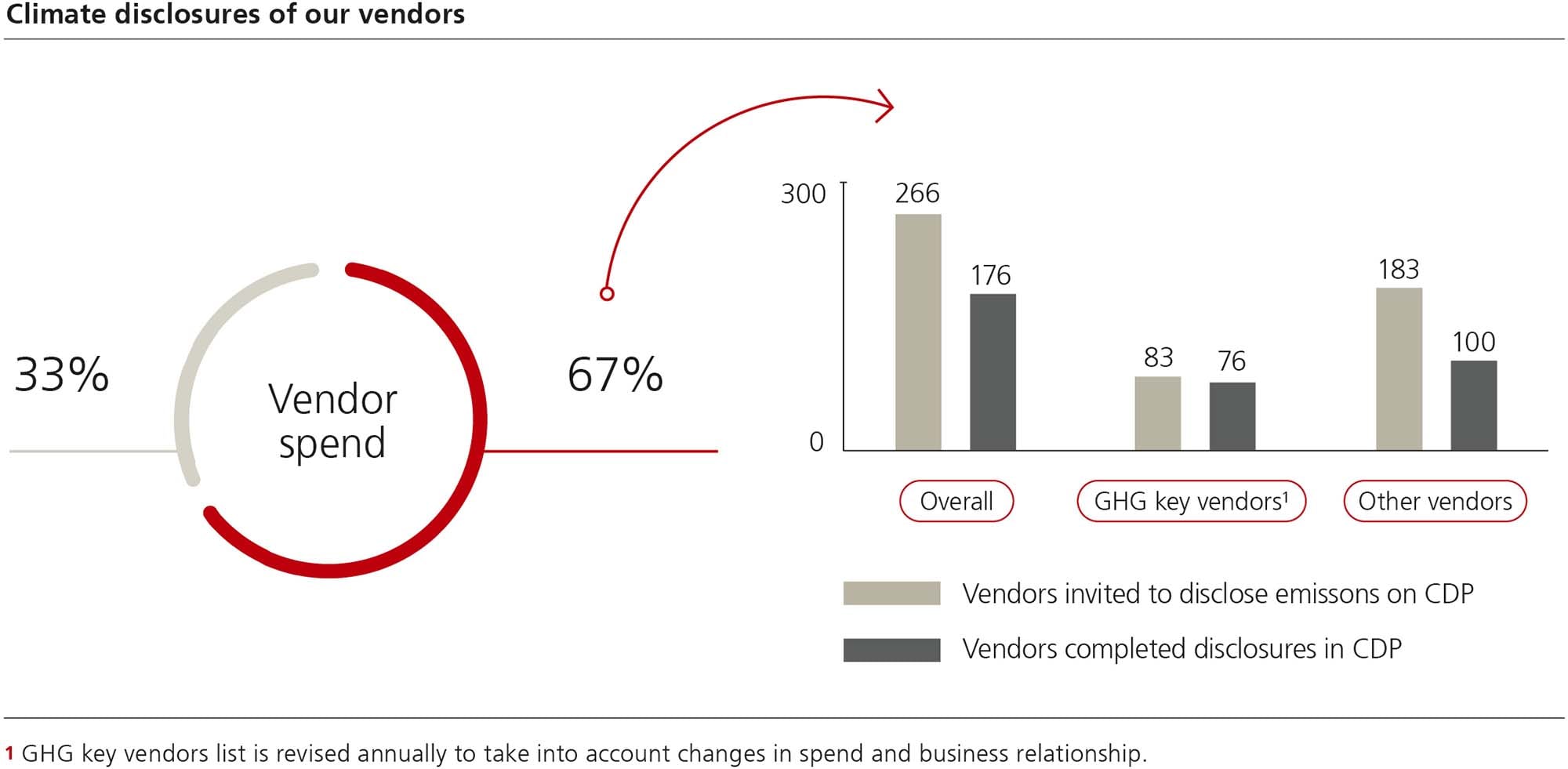

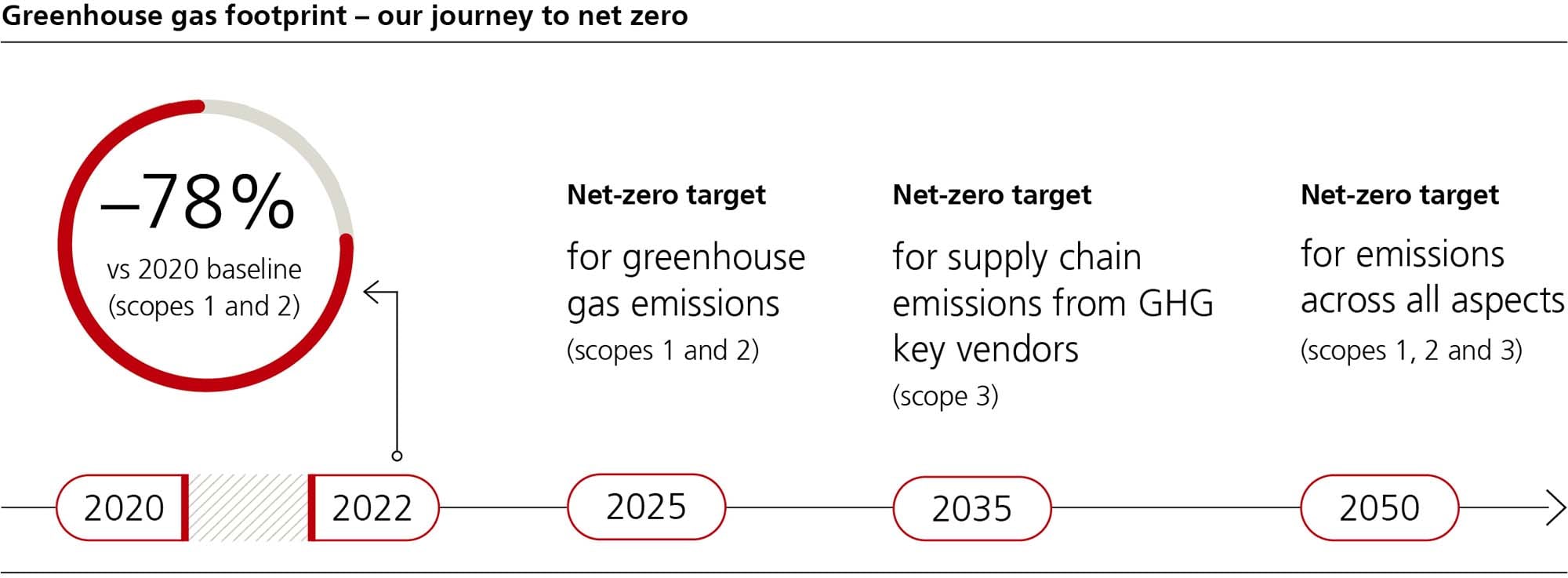

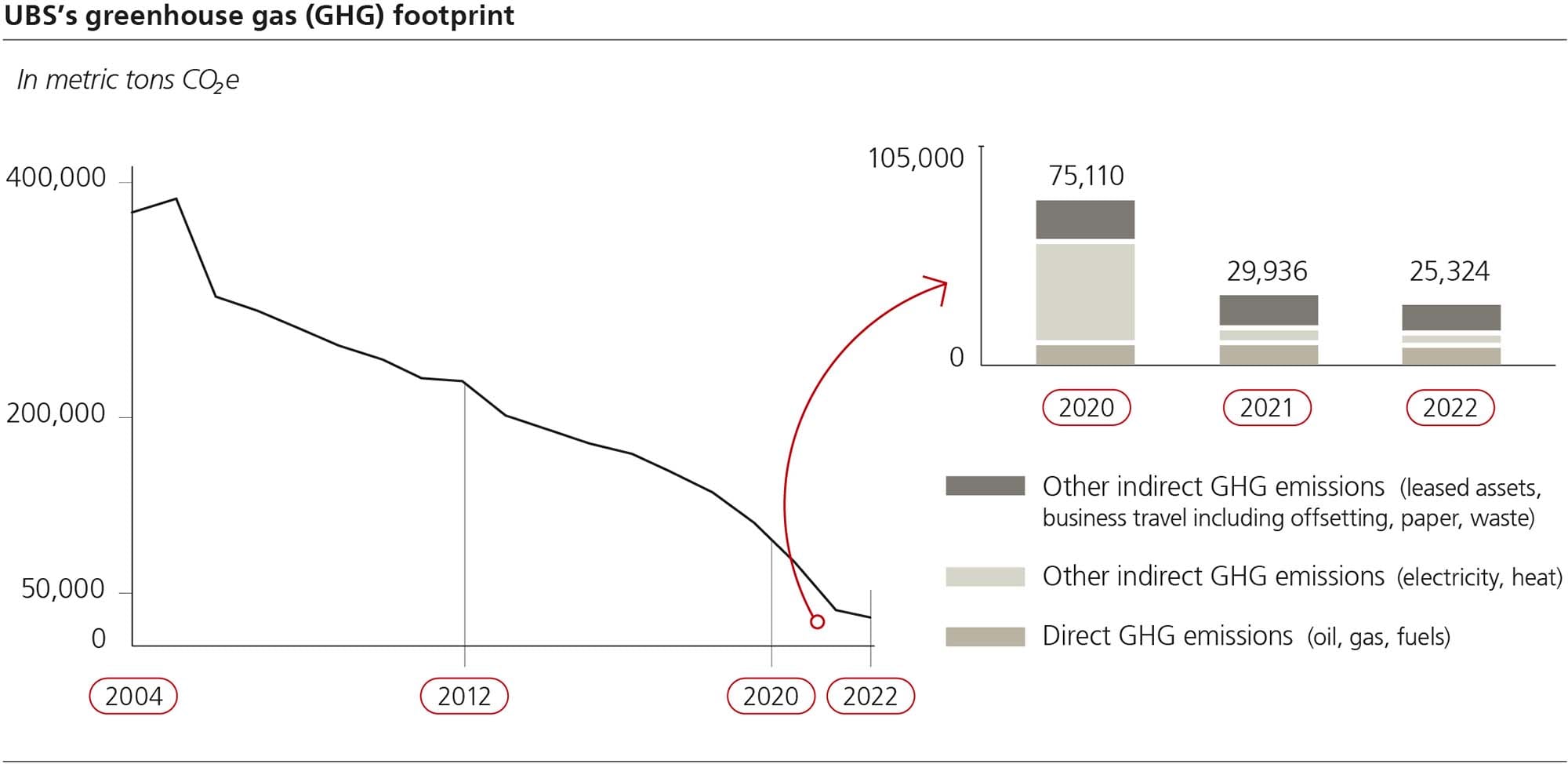

Direct climate impact: In 2022, we reduced our scope 1 and 2 emissions by 13%. We also identified “GHG key vendors,” that collectively account for more than 50% of our estimated vendor GHG emissions. We invited the vendors that accounted for 67% of our annual vendor spend to disclose their environmental performance through CDP’s Supply Chain Program. 66% of those invited completed these disclosures.

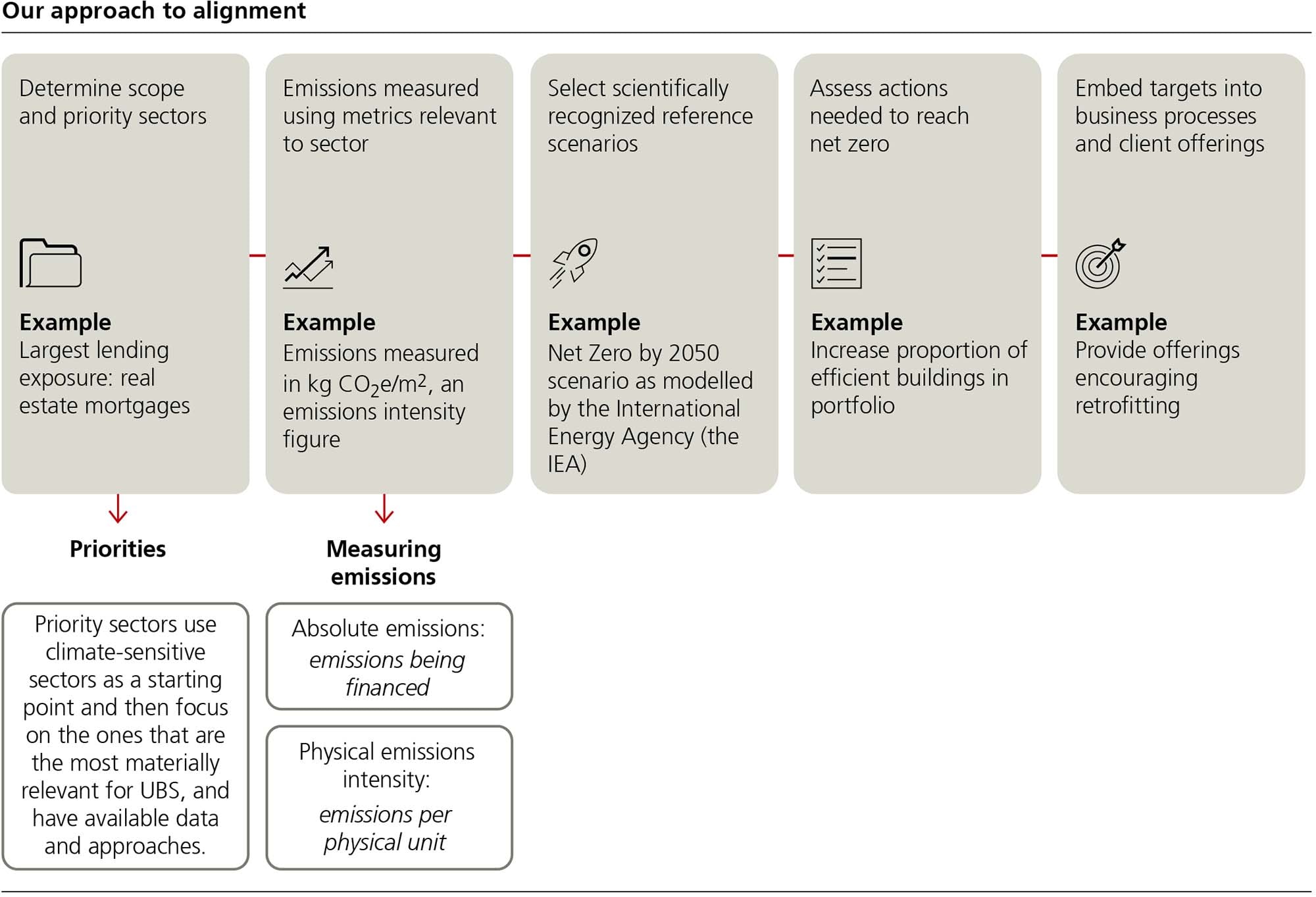

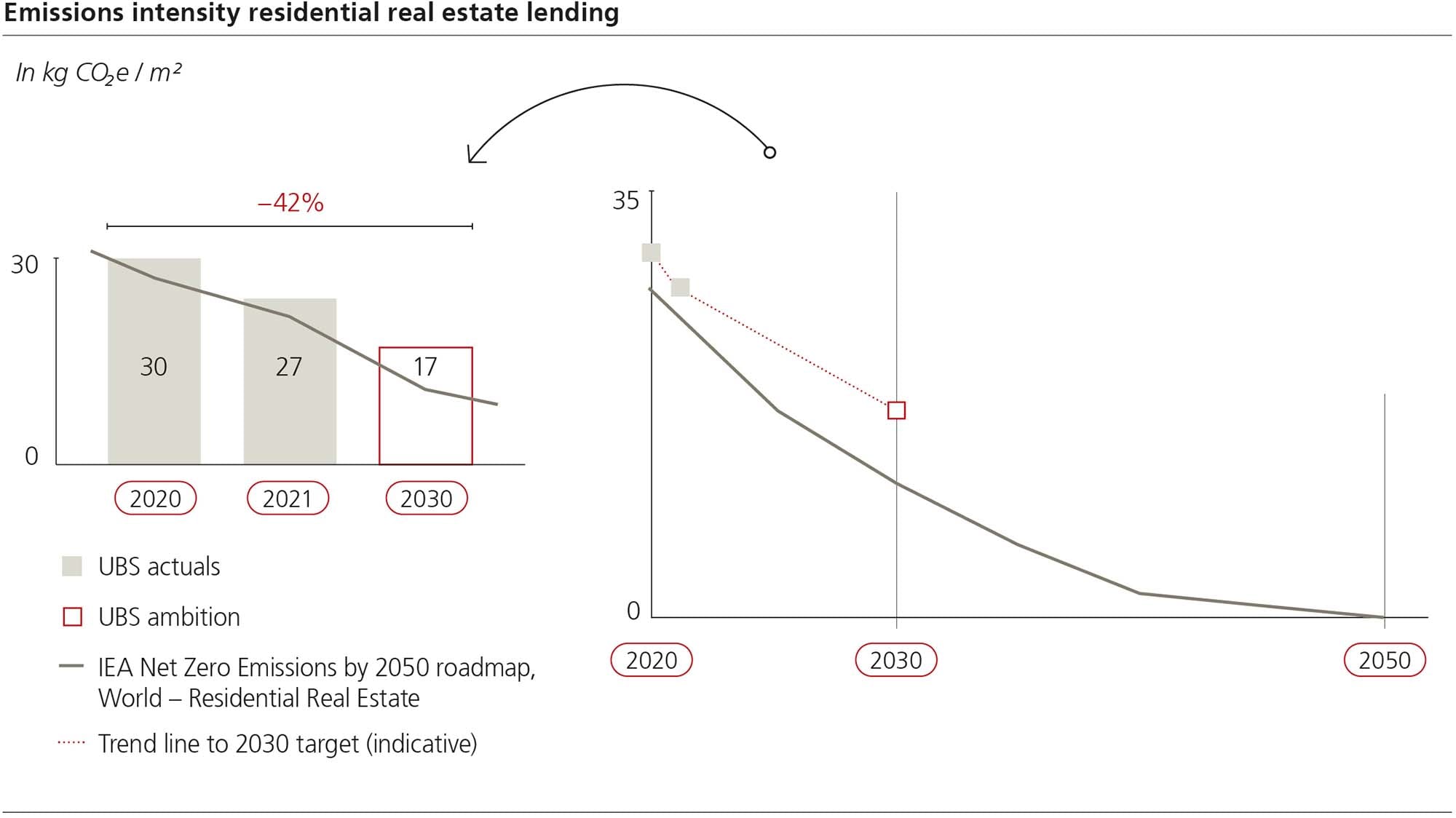

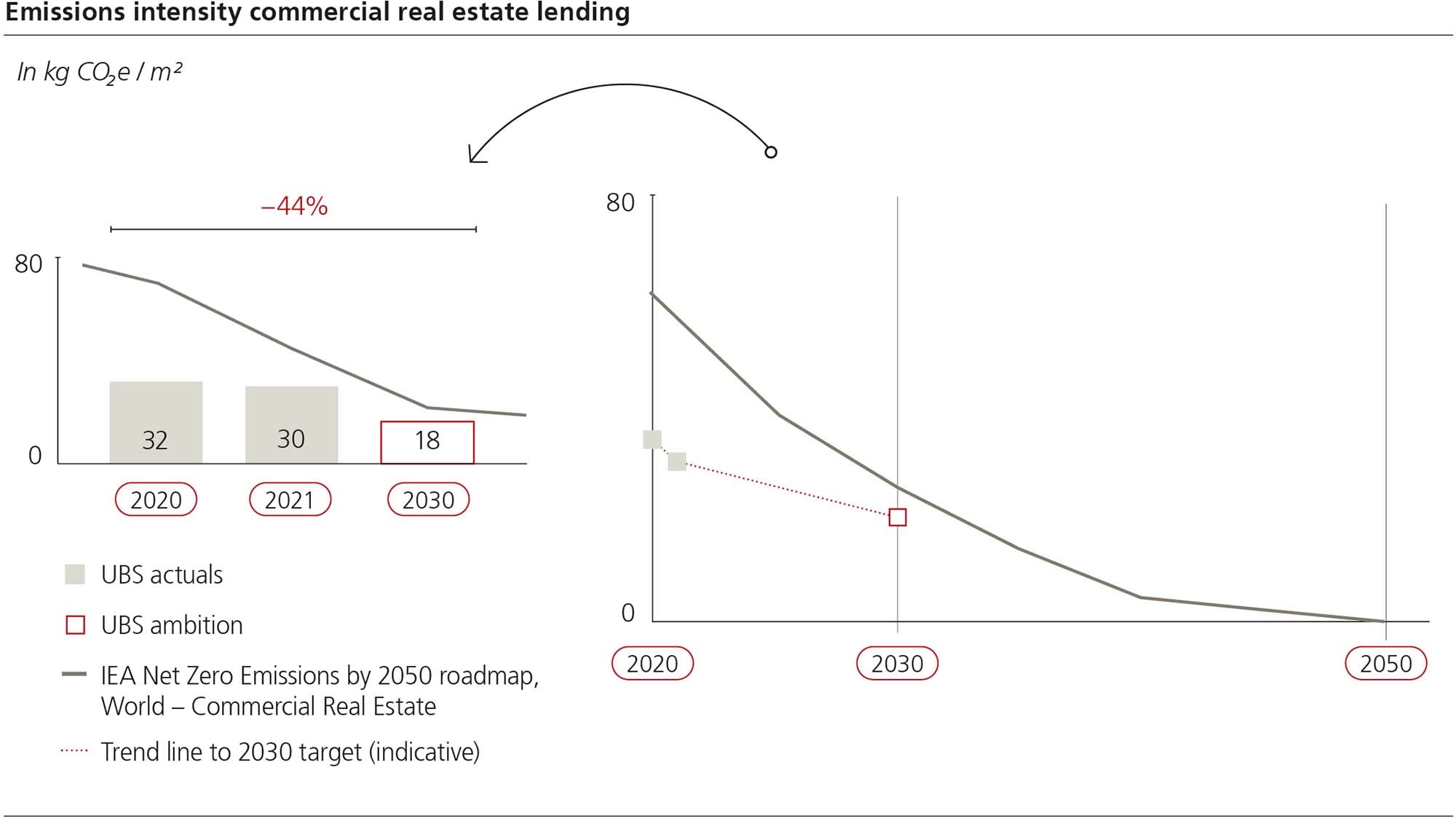

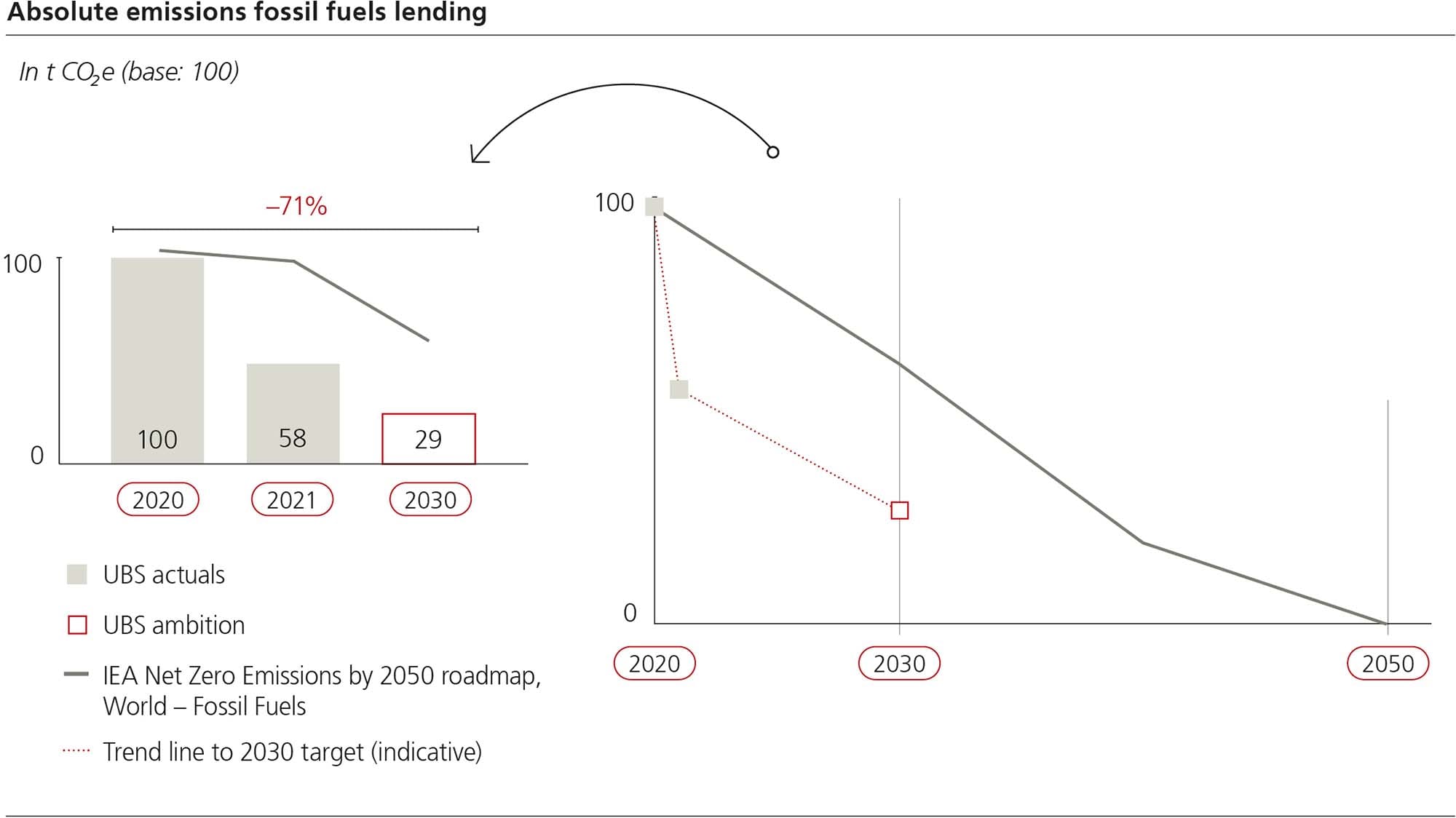

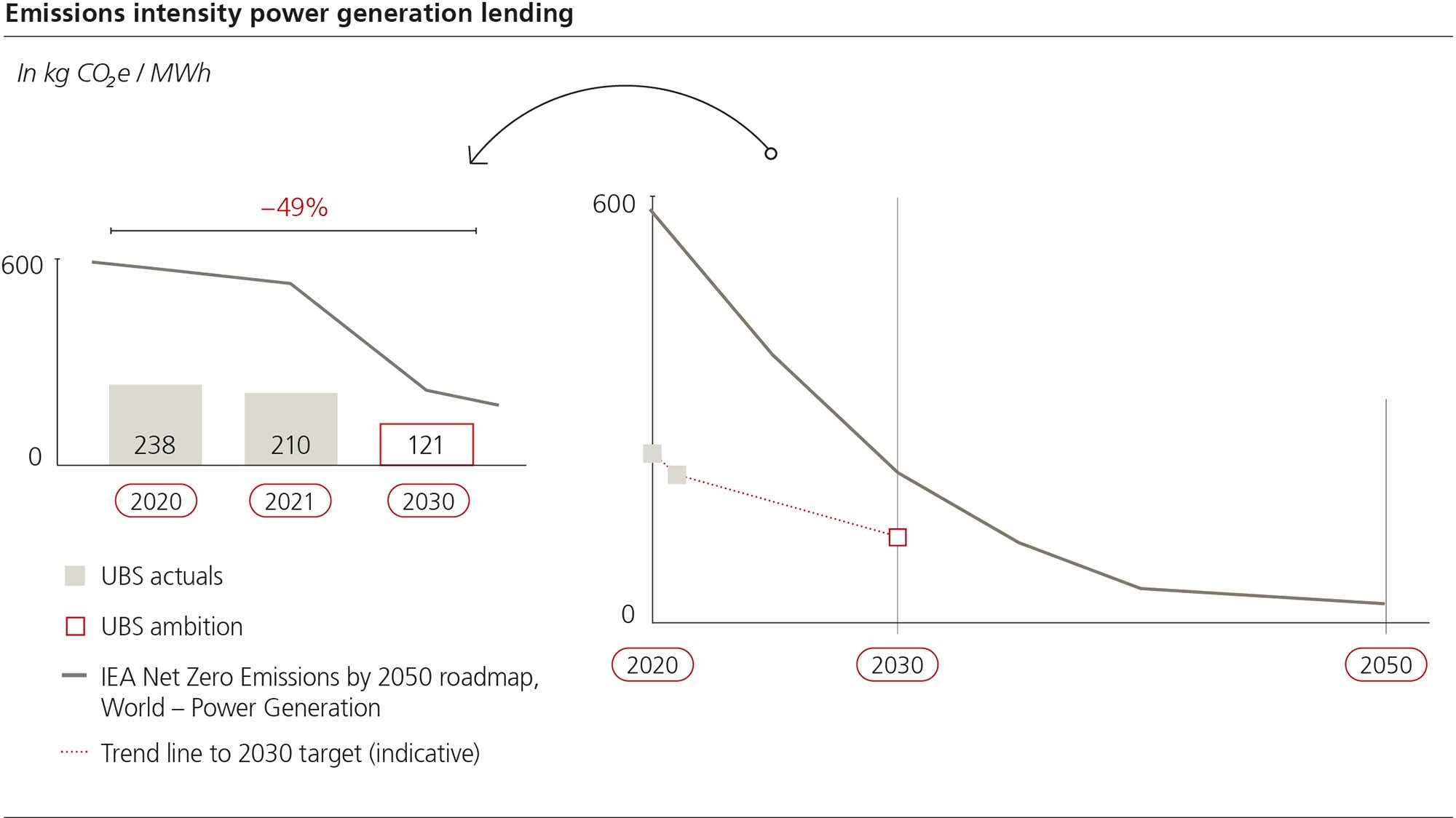

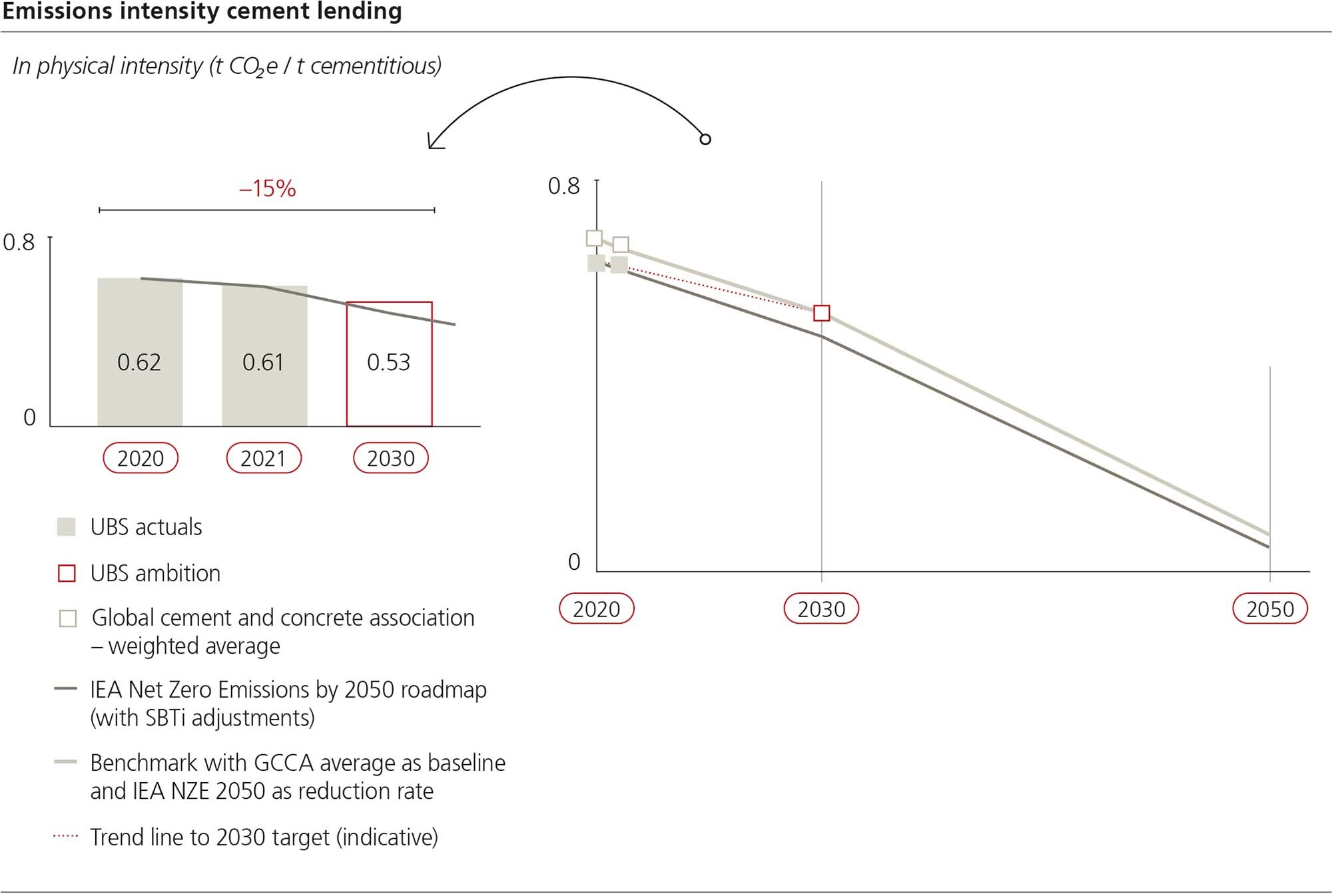

Financing activities: We have established interim goals aligned with this objective for real estate lending across all of our business divisions and for other financing activities in our Investment Bank and our Personal & Corporate Banking. In 2022, we defined cement as a further net-zero target sector and added it to the scope of our roadmap for the Investment Bank and Personal & Corporate Banking. We also undertook further assessment of the overall emissions associated with UBS’s corporate lending and real estate mortgages. We intend to set additional goals for financing activities across all of our business divisions as appropriate data and methodologies are developed.

Investing: In 2022, our Asset Management business division made progress across the foundational pillars required to deliver its target of aligning 20% of total assets under management (AuM) to be managed in line with net zero by 2030.i This included enhanced data sourcing and governance, developing asset-class-specific net-zero-aligned frameworks, and extending our long-standing climate engagement program. In 2023, Asset Management intends to implement revisions to fund documentation and investment management agreements to align with these updated frameworks. Our Global Wealth Management business division will develop plans to expand its solutions offering to enable clients to achieve their net zero objectives. In 2022, Global Wealth Management continued to leverage its knowledge and industry partnerships to explore and develop carbon-focused offerings.

Refer to the “Appendix 4 – Metrics and targets” section of this report for our climate-related methodologies Refer to “Our transition plan” in the “Appendix 4 – Metrics and targets” section of this report for a high-level overview of our activities to support our own transition and that of our counterparties in the real economyOur climate roadmap

Reducing our environmental footprint

We are working to minimize our own operational footprint and support our employees, clients, suppliers and investors in the decarbonization of their activities. By ensuring extensive and accurate reporting of the progress to reduce greenhouse gas (GHG) emissions, we are laying the groundwork for transparent monitoring by our stakeholders. Energy aside, our other environmental focus areas are water, paper, waste and travel.

Environmental focus areas

Energy reduction and sustainable buildings

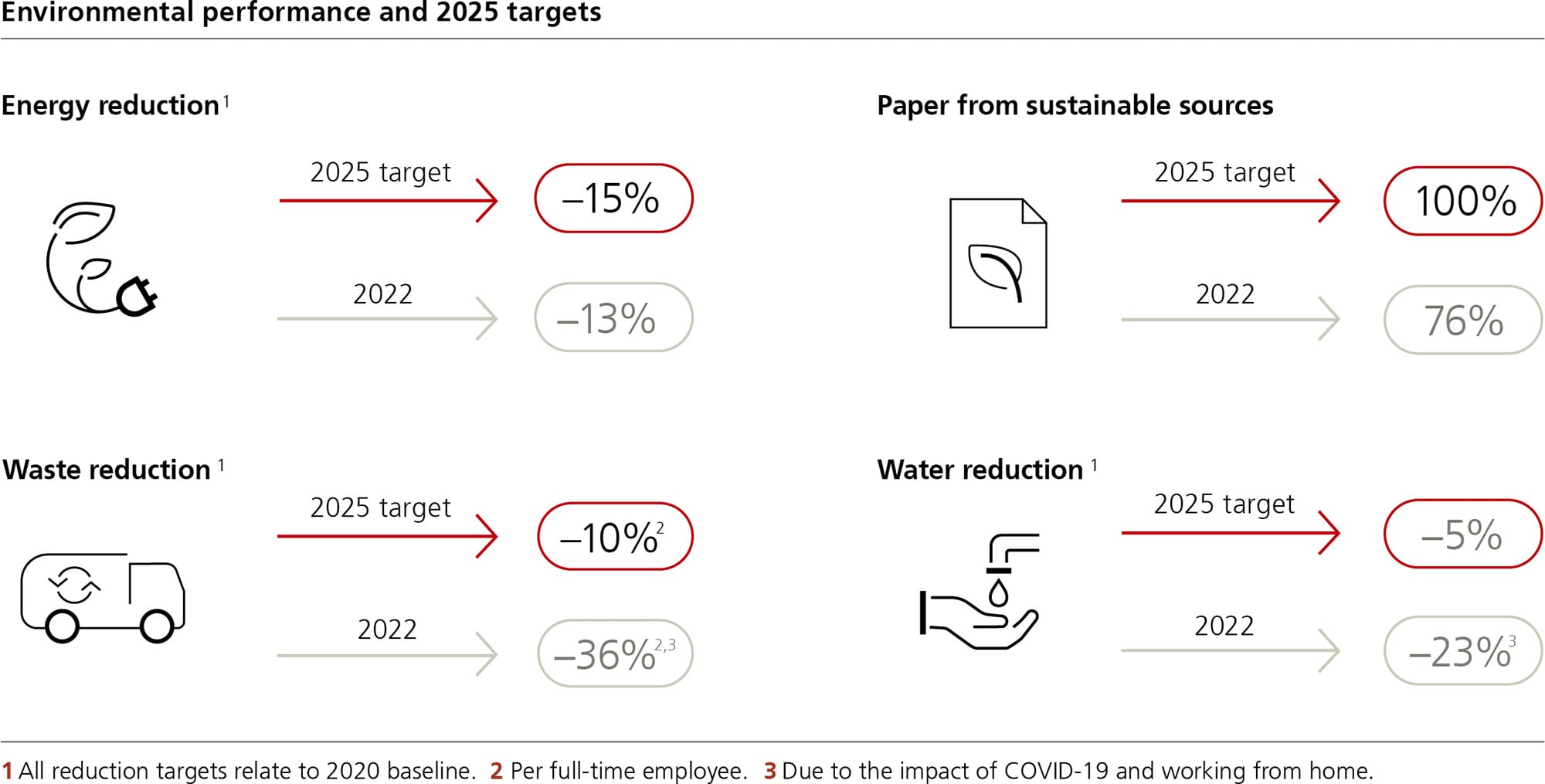

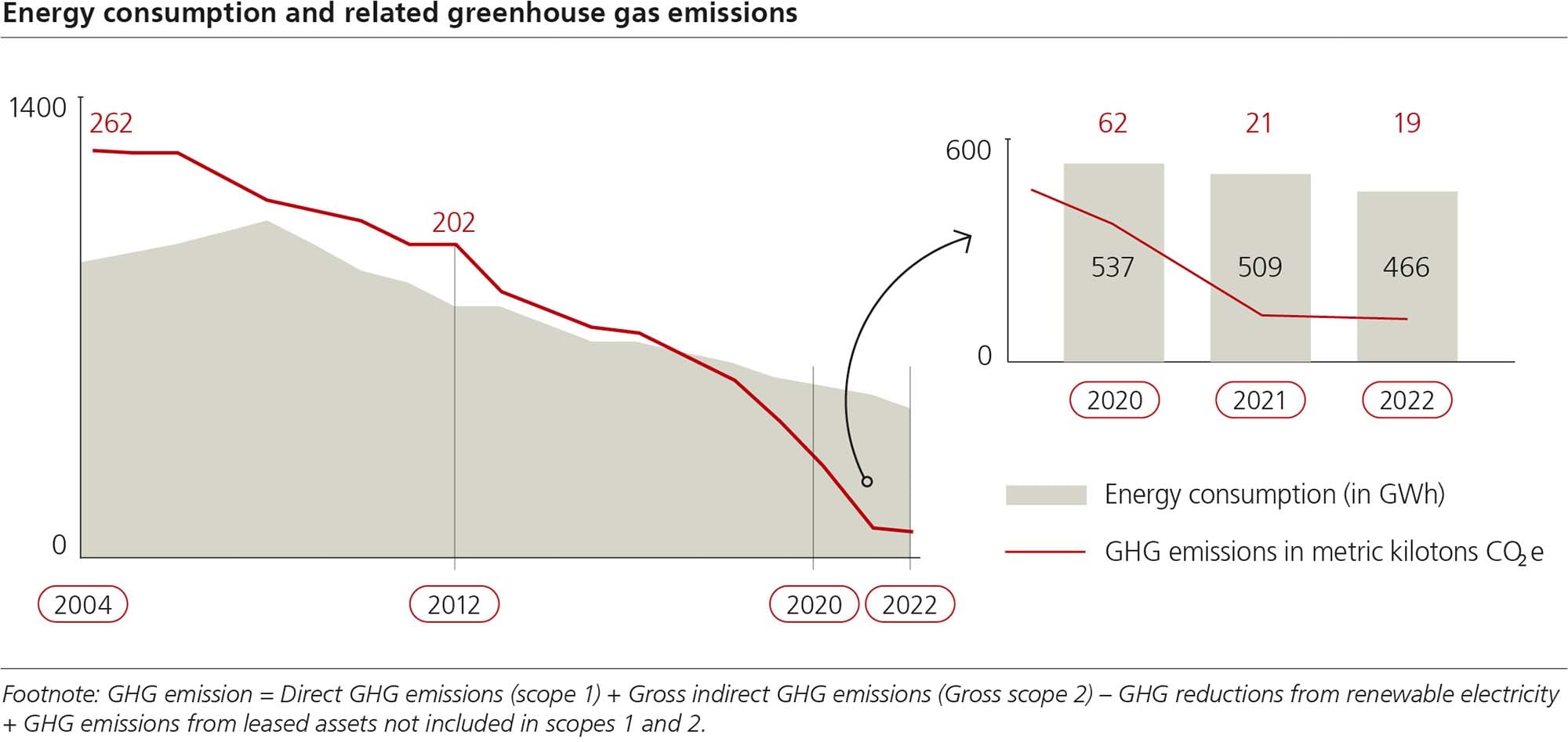

We have stepped up efforts to reduce our operational energy consumption while also improving the efficiency of our corporate real estate portfolio. We achieved an energy consumption reduction of 8% in 2022, compared with 2021. Several different initiatives contributed to this reduction, for example, reducing our global real estate and data center footprint, investing in more sustainable buildings and upgrading existing buildings by switching to energy-saving LED lamps and replacing pumps, heating systems and other equipment. We also installed solar panels on 3 buildings during 2022. These measures led to a reduction of 13% in our scope 1 and 2 emissions compared to the previous year.

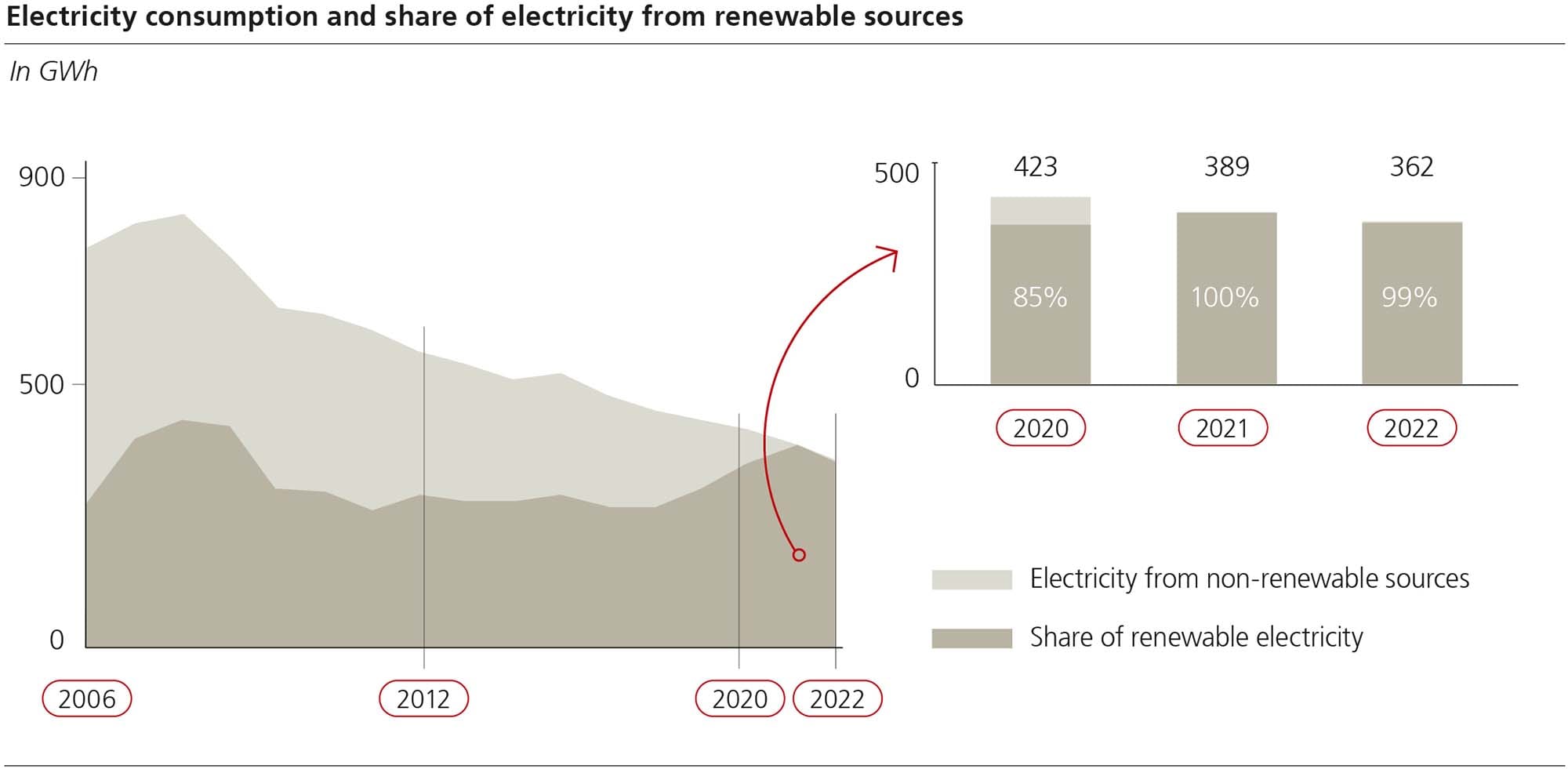

We remain committed to sourcing 100% renewable electricity across our operations globally. For 2022, despite challenging circumstances, we achieved 99% in line with RE100 initiative requirements.i We have taken further steps to decarbonize our operations. Several locations have been certified to internationally recognized green-building standards, including our office in Shenzhen. It achieved the highest score for LEED Platinum v4 globally at the time of certification (October 2022). To ensure our buildings adhere to such high standards in the future, we have designed and are implementing a new internal benchmark to rate potential real estate options based on their environmental impact and sustainability. This benchmark was built on foundations from international standards such as Leadership in Energy and Environmental Design (LEED), the Building Research Establishment Environmental Assessment Method (BREEAM) and Green Mark.

For more details on LEED certifications refer to usgbc.org/projectsFor the transition period to net-zero scope 1 and 2 emissions by 2025, we have purchased high-quality nature-based carbon offsets to compensate for our current net emissions. From 2025 onward, we expect there will be a residual amount of emissions that cannot be fully mitigated. We have therefore contracted over 80,000 metric tons of permanent carbon removal, of which we anticipate needing 8,000 to 10,000 metric tons per annum. Our commitment to the very highest standards of permanent carbon removal also creates an implied internal cost of carbon of approximately USD 400 per metric ton for scope 1 and 2 emissions and provides a strong reduction incentive, for instance on investment cases that seek to eliminate fossil fuel heating systems.

Reducing water, paper and waste

We regard the reduction of water consumption as a key priority. With many countries experiencing severe droughts in 2022, the urgency is clear. Some of the efficiency measures we took included the use of aerator taps, waterless urinals, new mixing valves and WaterSense-certified showerheads. As a result, we were able to retain the low level of water use from 2021 and avoid an expected increase from higher employee presence in our offices.

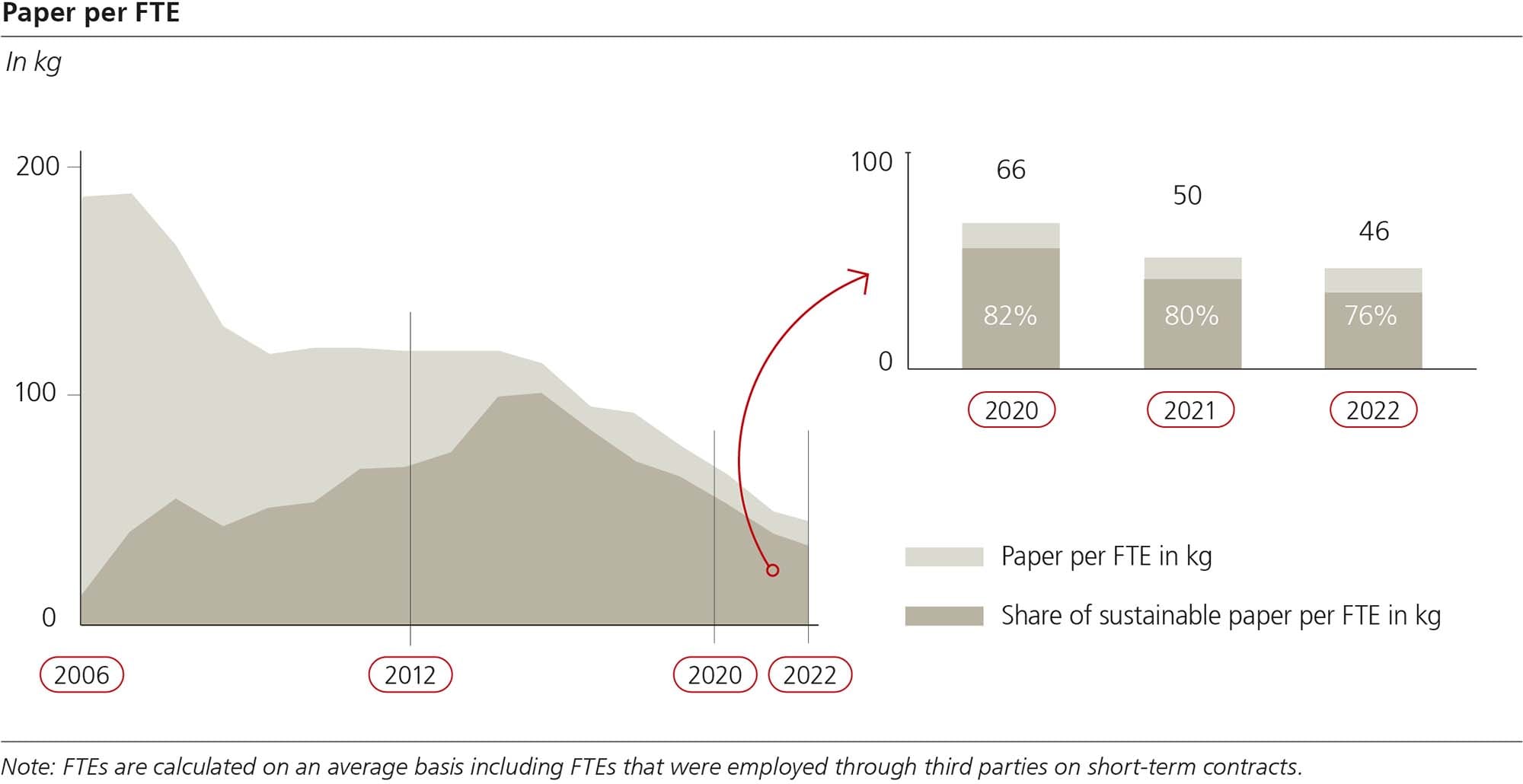

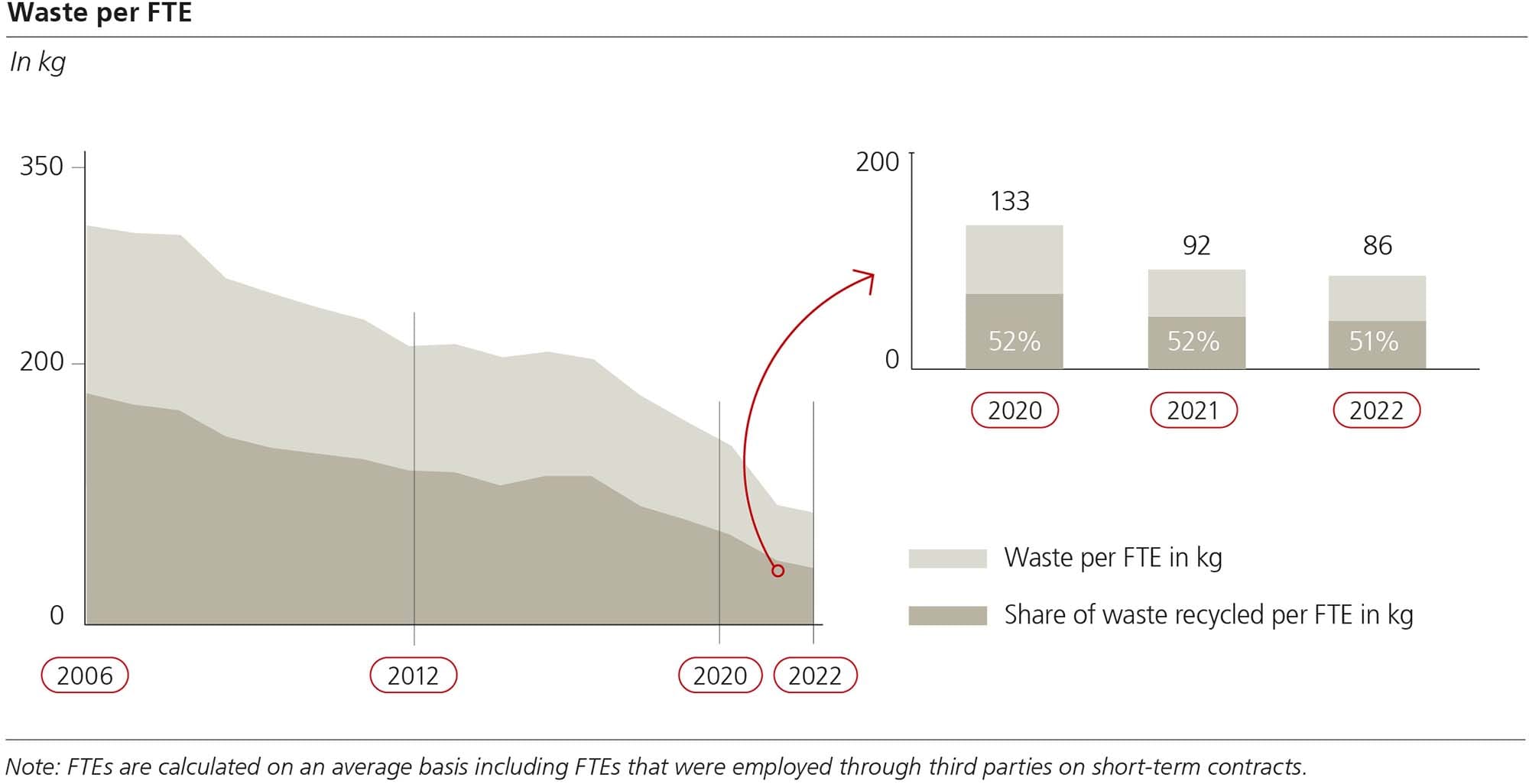

We reduced paper consumption per full-time equivalent (FTE) by 8% compared to 2021 through our #ZeroPaper campaign. We achieved this by an ongoing reduction of the number of printers in our offices and several employee awareness campaigns. In addition, our firm’s employees have continued their reduced printing habits when returning to the office after the pandemic. We also launched a concerted effort to map all our paper-intensive processes and find alternatives. Our paper usage consists of 21% copier / printer paper, 52% client output and 8% publications, with the remainder coming from various paper products. The share of paper sourced either from recycling, or paper certified by the Forest Stewardship Council (the FSC) was 76%.

We eliminated takeaway packaging at selected locations, as part of our efforts to reduce our waste production. This resulted in an elimination of 650,000 single use items per year. This supported a general waste reduction per FTE by 6% compared to 2021. We also cut landfill waste by 1% compared to the prior year, to approximately 2,300 metric tons globally.

Travel

We see travel activity returning again after the pandemic. Through our travel policy, we actively promote video conferencing and other collaboration tools as a first option to reduce air travel. Secondly, we focus on the means and frequency of travel and work to change mindsets and traveler behavior. During 2022 we introduced CO2 emissions as a key metric on all business-reporting dashboards and introduced emissions metrics at the time of booking to support more sustainable travel through lower carbon options such as train rather than air travel. Among our preferred hotels are those that have met certain sustainability criteria. These have a green flag credential that is visible at the time of booking to aid bookers in their decision-making. We continue to purchase high-quality carbon offsets that correspond with 100% of our air travel emissions.

Biodiversity

We introduced measures to improve biodiversity, for example through the installation of new beehives at some of our office locations and tree planting initiatives across Europe. We also introduced an annual “Clean-up day,” during which UBS volunteers took part in a coordinated effort to clean up street litter in their respective cities.

Emissions in our value chain

We recognize the importance of better understanding the emissions resulting from our value chain. For scope 3, category 1, we have made a first estimation, which enabled us to identify the top contributors and design a program for their engagement.

Refer to “Monitoring the environmental impact of our supply chain” belowWe are also looking to quantify any relevant scope 3 emissions from categories 1 to 14, for instance employee-related ones resulting from working from home and commuting.

Our environmental management system (EMS)

All our environmental activities, including the entire scope of UBS products, services and in-house operations, are subject to our EMS, which we run in accordance with ISO 14001:2015. We have done so since 1999, when we were the first bank to obtain this certification for our worldwide EMS. Since then, we have successfully passed the ISO 14001 audits every year. Additionally, in the EU and the UK we are certified according to the energy management system standard ISO 50001:2018. Information on our environmental indicators (energy, water, paper, waste, recycling and travel) and associated GHG emissions is externally verified on the basis of the ISO 14064:2018 standard. These three sets of comprehensive audits confirm the appropriate policies and processes are in place to manage environmental and energy topics in our operations and that they are applied on a day-to-day basis.

Challenges

During the second half of 2022 the energy supply situation in Europe prompted us to introduce additional operational measures to decrease energy use generally and natural gas use specifically. Examples include lowering heating set-point temperatures, reduced comfort cooling in offices and tighter control of lighting. In line with government recommendations, we also switched from natural gas to oil to fuel some of our heating systems in Switzerland. Because our environmental reporting year is 1 July to 30 June, the result of these measures will be shown in our 2023 sustainability disclosure. While the energy reduction measures will have a positive impact on our energy usage, the temporary fuel switch will result in a modest increase in our emissions for that period. We remain committed to our net-zero scope 1 and 2 emissions goal for 2025.

Managing our supply chain responsibly

We embed environmental, social and governance (ESG) standards into our sourcing and procurement activities. Our firm-wide Responsible Supply Chain Management (RSCM) framework is based on identifying, assessing and monitoring vendor practices in the areas of human and labor rights, the environment (including aspects of nature), health and safety and anti-corruption. Central to our RSCM framework are our Responsible Supply Chain Standards (RSCS), to which our direct vendors are bound by contract. The RSCS define our expectations toward vendors and their subcontractors regarding legal compliance, environmental protection (including aspects of nature), avoidance of child and forced labor, non-discrimination, diversity, equity and inclusion, remuneration, hours of work, freedom of association, humane treatment, health and safety, anti-corruption measures, and whistleblowing protection for employees.

In 2022, we revised our RSCS and raised the bar for ourselves and our suppliers.Refer to our RSCS, available at ubs.com/suppliers

Monitoring the environmental impact of our supply chain

We are strengthening sustainable practices and engaging with many of our suppliers on climate information disclosures to create transparency and commitment toward the reduction of GHG in our supply chain. In 2021, we received external recognition for our efforts through the CDP Supplier Engagement Leaderboard.

In 2022, we identified “GHG key vendors,” which we define as those vendors that collectively account for >50% of our estimated vendor GHG emissions. We then invited the vendors that accounted for 67% of our annual vendor spend to disclose their environmental performance through CDP’s Supply Chain Program. This included all GHG key vendors. We implemented a structured communication plan, conducted webinars to guide our vendors through the disclosure process and requirements, and met with all the GHG key vendors to ensure they understood the need for and importance of declaring their emissions and committing to their own net-zero targets.

The results have been very positive, with 66% of the invited vendors completing their climate disclosures in the CDP platform. This not only enables us to develop tailored engagement plans based on the maturity of the vendor, it also provides a vital input for us to establish a baseline for supply chain vendor scope 3 emissions and identify focused emissions reduction initiatives. In 2023, we plan to extend CDP to a further set of vendors, thereby expanding coverage across our supply chain.

Refer to the “Appendix 4 – Metrics and targets” section of this report for details on the methodology applied

Engaging in sustainable technology

Leveraging the power of knowledge of our technologists

The Group-wide Sustainable Technology Guild (the STG) of our Chief Digital and Information Office (the CDIO) aims to raise awareness among our firm’s technology teams of sustainable technology initiatives and accelerate the execution of strategic plans that will have a positive environmental impact. The STG also contributes to our firm’s net-zero-by-2050 ambition by rethinking ways that we develop and deploy applications, store data and manage our firm’s infrastructure to fully offset legacy CO2 emissions in CDIO Technology.

Staffed by a volunteer community of UBS employees, the STG has expanded and now includes subject matter experts, such as key talent technology engineers and business influencers,i who have a strong interest in sustainable technology. Backgrounds range from software development to infrastructure engineering, cloud computing, real estate expertise, initiative management and communications.

The STG has been focusing on four distinct tracks, all of which are sponsored by our firm’s senior management:

- Optimization of our on-premises technology estate to support more energy-efficient consumption, by continuous decommissioning of unused and power-intense technology components, as well as changes to hours of operations;

- application development with sustainability in mind, achieved by providing transparency, using near real-time metrics, to application owners about the environmental impact of their applications;

- execution of our Cloud First strategy and continuous adoption of our primary strategic Cloud partner, Microsoft; and

- optimization of projects, process, production environment and people by running internal campaigns to encourage employees to clear up their archives and the applications and systems that they are accountable for.

Across all these initiatives, CDIO Technology continues to upgrade our firm’s technology infrastructure with newer and more efficient, market-leading infrastructure and technology vendors, moving some technology platform workloads from its on-premises and private cloud servers to Microsoft Azure yielding energy reductions of, in some specific use cases, up to 30%.

We have joined the Green Software Foundation (the GSF), as part of our ongoing commitment to drive more sustainable practices. As a GSF steering member, we explore ways of reducing emissions associated with our large technology estate. For example, UBS and Microsoft co-developed a Carbon Aware API. This open-source solution recommends scheduling workloads requiring heavy computer power during times when clean, renewable or low-carbon sources of electricity are most available. Both firms then provided this solution to the GSF so it could be shared with large and small companies around the world.

Driving social impact

As we continue to drive our social impact and philanthropy services strategy forward, we are building a strong platform for the future. We seek to grow our reach and maximize our impact on a local, national and global scale.

Philanthropy Services

We believe that by working collectively, philanthropists and public and private organizations have the potential to create lasting change and maximize a positive impact for people and planet. UBS Philanthropy Services provides comprehensive advice, insight and execution services to work with our clients and find innovative ways to tackle some of the world’s most pressing social and environmental problems. To support our clients we have also issued various publications such as the philanthropy guides: Sea beyond the Blue, Seeds of Change, and On Thin Ice.

The UBS Optimus Foundation network

In many cases investing in nature also requires partnerships and strategic collaboration. As an example, the UBS Optimus Foundation network and the Swiss Agency for Development and Cooperation supported the issuance of two reports by Earth Security: The Blended Finance Playbook for Nature-Based Solutions and Financing the Earth’s Assets: The Case for Mangroves. These reports outlined approaches to nature-positive investments using blended finance structures that leverage philanthropic capital. We took this a step further toward moving from concept to solution in 2021 with the creation of the Mangrove 40 initiative to support nature-based solutions for carbon sequestration via the restoration of mangroves, designed to provide environmental and social co-benefits.

The work with Earth Security has identified 40 locations globally that contain 70% of the world’s remaining mangroves, of which approximately 50% have been degraded. Mangrove ecosystems store carbon faster than land forests, protect coastlines and restore biodiversity, and they can also support local livelihoods. This demonstrates the UBS Optimus Foundation network’s strengthened focus on climate and the environment, as well as the power of philanthropy to catalyze nature-based solutions and help create new nature markets.

2022 highlights include:

Collective impact

- Members of the Accelerate Collective, Climate Collective and Transform Collective entered their second year of collective impact and learning, including in-person summits.

- Through the UBS Climate Collective, for example, clients are able to fund, develop and implement strategies that target climate change mitigation and adaptation, and may also serve to support natural capital.

- We signed a memorandum of understanding with Prince Albert II of Monaco, creating a new USD 2 million program within the Pelagos Initiative, which is accelerating climate action in the Mediterranean.

- In partnership with the Galileo Foundation, we launched the Human Family Fund at the Faith and Philanthropy summit at the Vatican, which is a multi-faith philanthropic fund supporting faith-inspired initiatives with verified outcomes in health, education, climate / environment and anti-trafficking.

- We formed a new strategic partnership with the Marshall Institute and LSE (London School of Economics).

Donor-advised funds

These funds offer clients an easy, flexible and efficient alternative to setting up their own foundation and can be managed in line with their usual investment approach.

UBS Global Visionaries

To further grow our environmental and social impact, we see an opportunity to connect people, to bridge the gap between incubation, acceleration and impact investments, supported by a strong ecosystem and partnership approach. One way we are doing this is through our UBS Global Visionaries program, where we aim to (i) create opportunities for clients and prospective clients to connect with leading social entrepreneurs and (ii) help the best entrepreneurs focusing on social and environmental issues to scale their positive change by expanding their network, building capacity and raising awareness about their work.

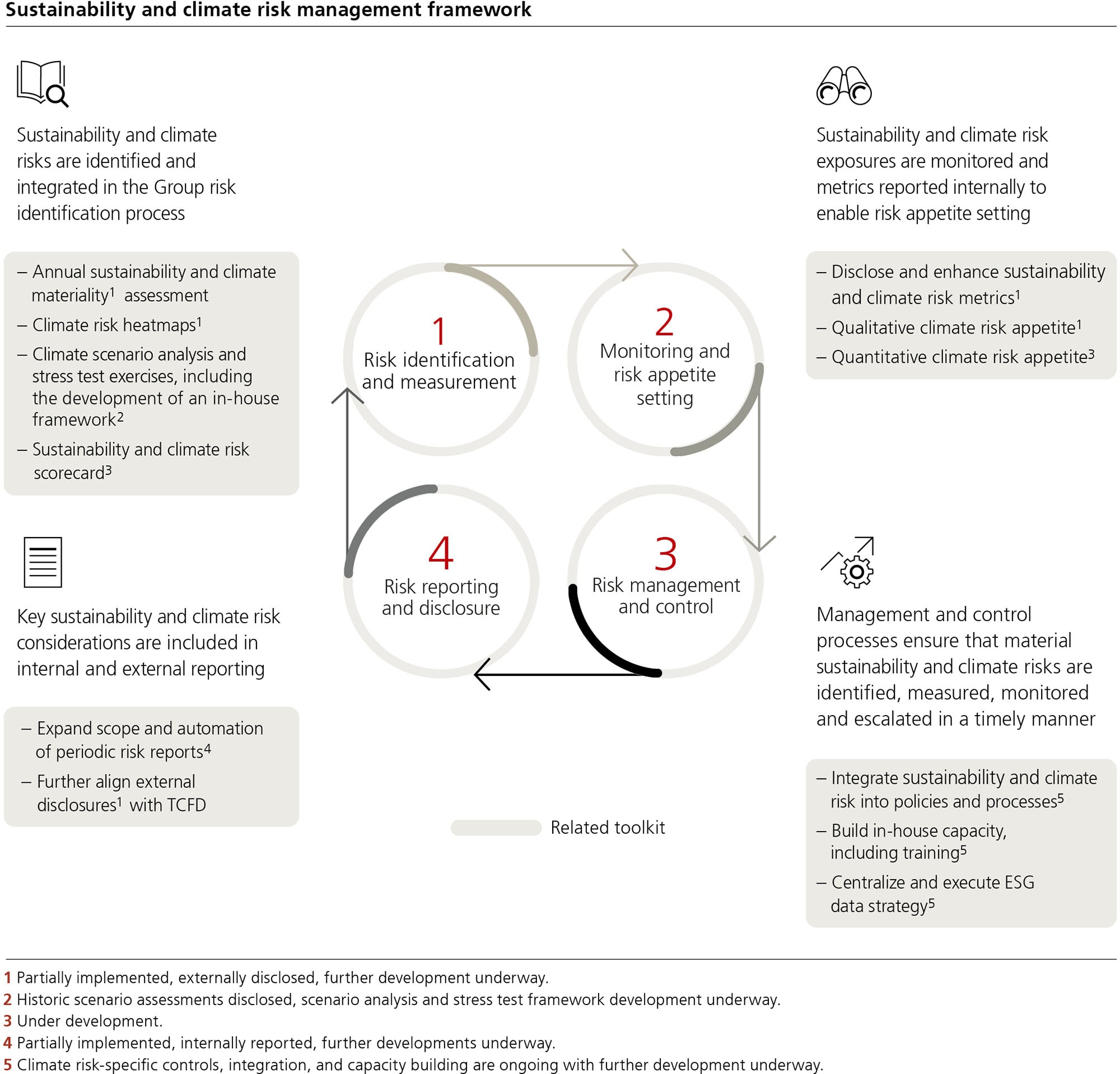

Risk Management

Managing sustainability and climate risks

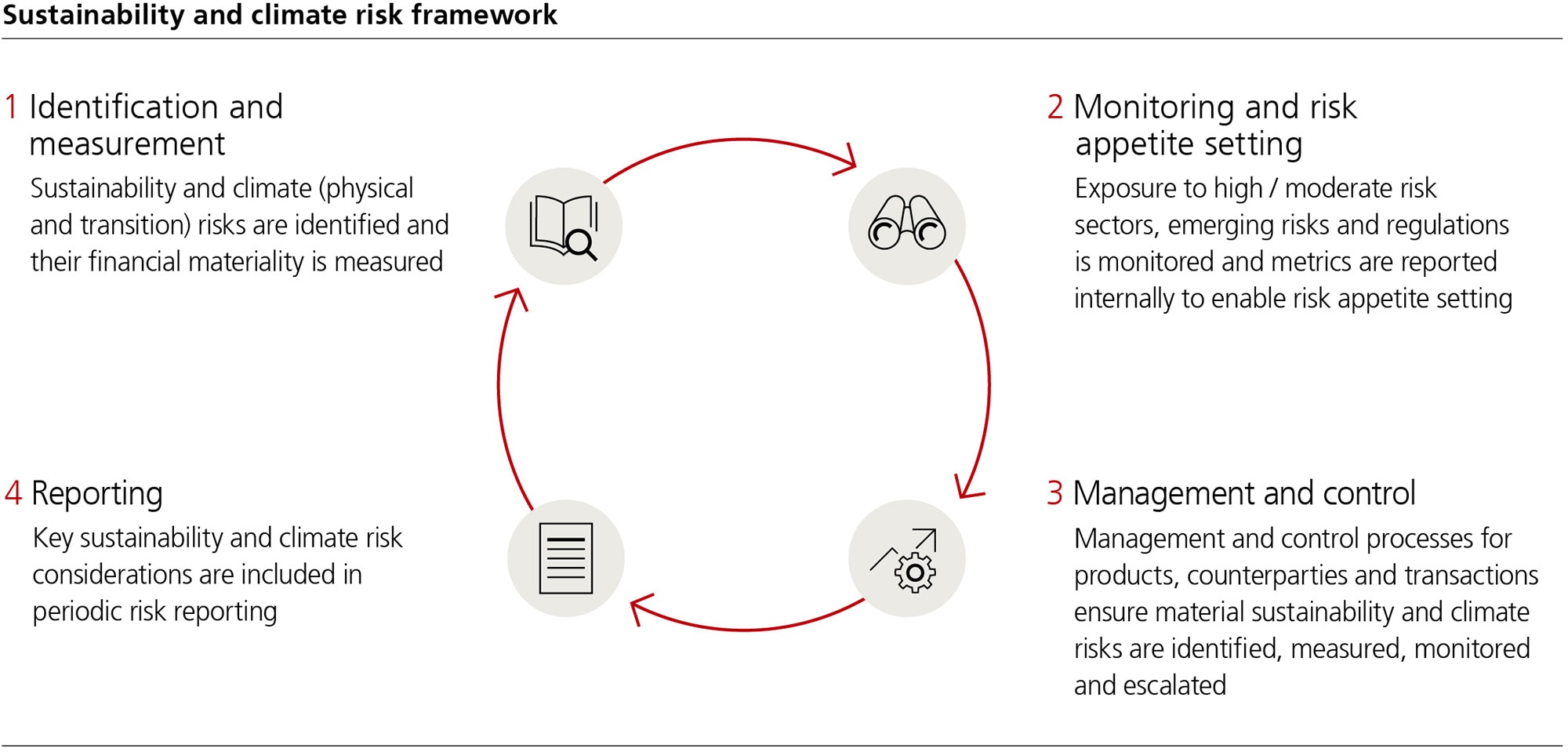

At UBS, sustainability and climate risk is defined as the risk that UBS negatively impacts, or is impacted by, climate change, natural capital, human rights, and other environmental, social and governance (ESG) matters. Sustainability and climate risks may manifest as credit, market, liquidity and/or non-financial risks for UBS, resulting in potential adverse financial, liability and/or reputational impacts. These risks extend to the value of investments and may also affect the value of collateral (e.g., real estate). Climate risks can arise from either changing climate conditions (physical risks) or from efforts to mitigate climate change (transition risks). Physical and transition risks from a changing climate contribute to a structural change across economies and, consequently, can affect banks and the financial sector through financial and non-financial impacts.

The firm’s Sustainability and Climate Risk (SCR) unit (part of Group Risk Control), manages material exposure to sustainability and climate risks. It also advances our firmwide SCR initiative to build in-house capacity for the management of sustainability and climate-related risks.